SLC32-W2 || Real Life Problem Solving Challenge: Budget Planning

Hello friends and welcome to my blog. Budget planning is one of the ways we manage our finances to avoid unnecessary expenditure and to be able to take financial accountability into action. Join me this week as I share on how I plan my weekly or monthly budget.

How do you plan your weekly or monthly budget? Explain well. |

|---|

| working on my budget tracker |

|---|

I plan my monthly budget immediately after receiving my income. I first of all I list all my expected income sources and then categorize my expenses accordingly to their order of importance or priorities.

These are the simple steps I use.

Step 1: Calculate my total Income

For example:

- Salary/Business Income: ₦200,000

- Side Hustle Income: ₦50,000

Total Income = ₦250,000

Step 2: I List my Essential Expenses

| Expense Category | Amount (₦) |

|---|---|

| Tithe | 25,000 |

| Feeding | 60,000 |

| Transportation | 20,000 |

| Electricity/Data | 20,000 |

| House Rent Savings | 30,000 |

| Family Support | 20,000 |

| Savings/Investment | 50,000 |

| Miscellaneous | 20,000 |

| Total | 245,000 |

Step 3: Set Aside Savings First

I believe in paying myself first. Therefore, I remove money to my savings and investments first before spending on other items.

Step 4: Review Weekly

Every weekend, I compare what I have spent with what I budgeted to see if I stayed within my budget limit. Doing this weekly review helps me to avoid over spending while I also try to maintain financial discipline.

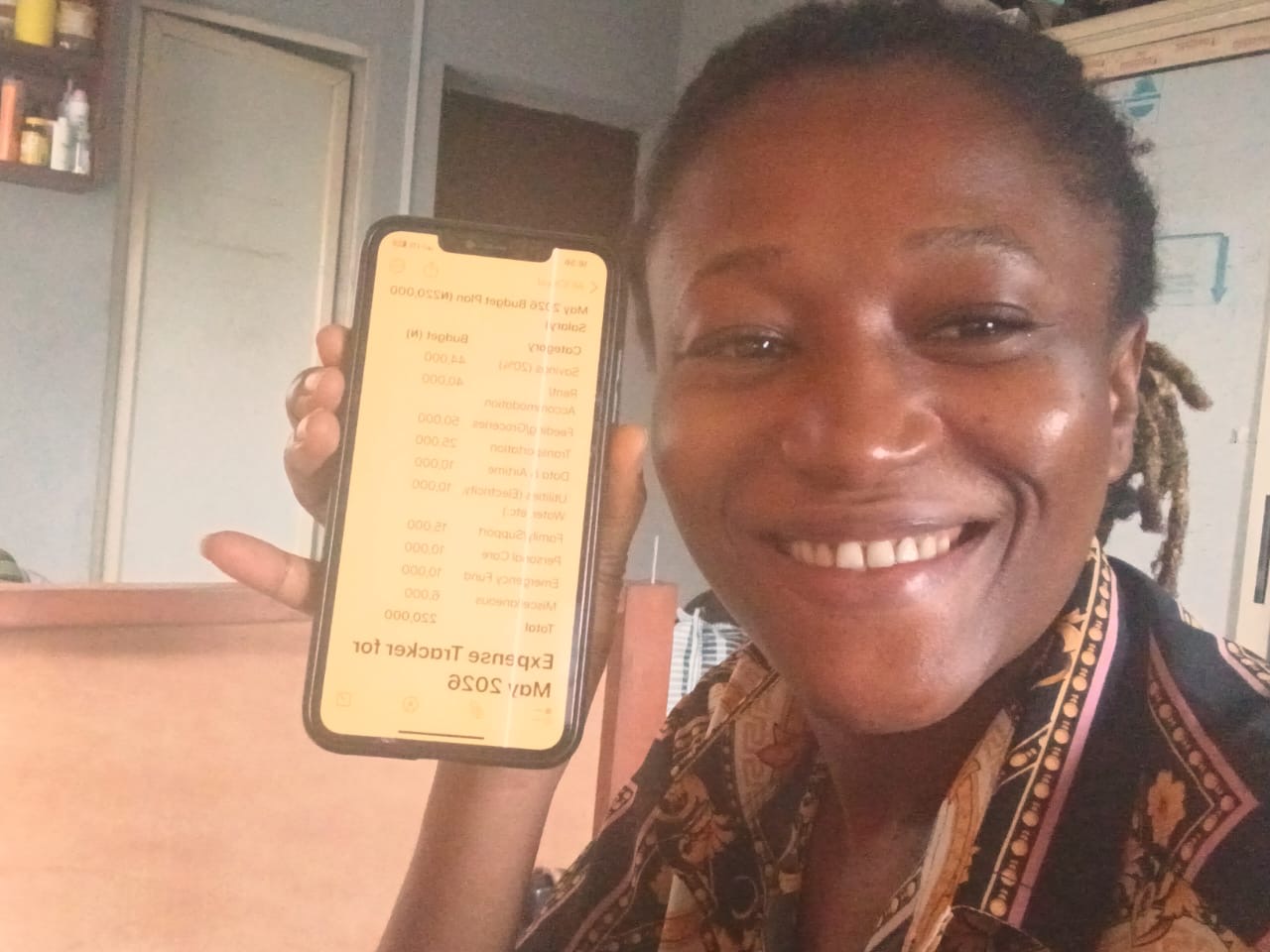

What tool or method do you use to track your expenses? Show at least one tool or method in detail with a selfie. |

|---|

To track my expenses, I primarily make use the Notes App on my phone.

Each day, I record the expenses I made no matter how small.

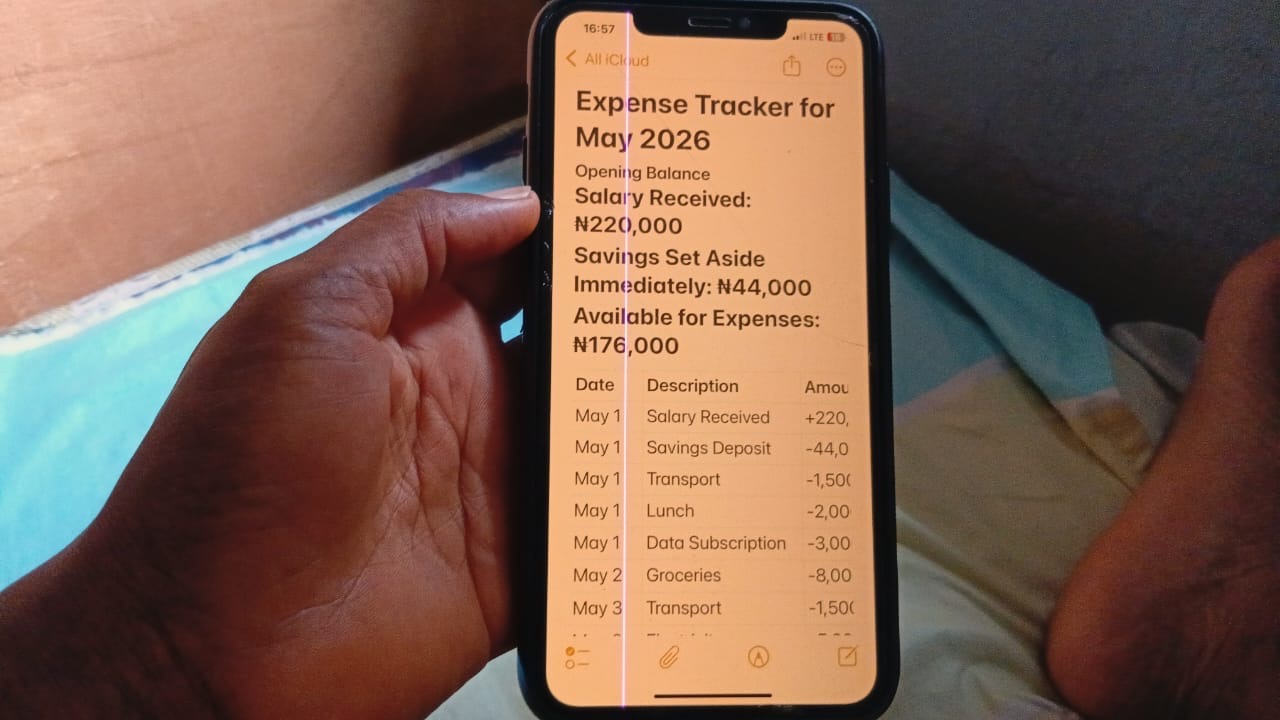

Example of how the expenses tracker looks on my phone note app.

Expense Tracker for May 2026

Opening Balance

Salary Received: ₦220,000

Savings Set Aside Immediately: ₦44,000

Available for Expenses: ₦176,000

| Date | Description | Amount (₦) | Balance (₦) |

|---|---|---|---|

| May 1 | Salary Received | +220,000 | 220,000 |

| May 1 | Savings Deposit | -44,000 | 176,000 |

| May 1 | Transport | -1,500 | 174,500 |

| May 1 | Lunch | -2,000 | 172,500 |

| May 1 | Data Subscription | -3,000 | 169,500 |

| May 2 | Groceries | -8,000 | 161,500 |

| May 3 | Transport | -1,500 | 160,000 |

| May 3 | Electricity Contribution | -5,000 | 155,000 |

| May 4 | Airtime | -2,000 | 153,000 |

| May 5 | Transport | -1,500 | 151,500 |

| May 5 | Household Items | -3,500 | 148,000 |

Etc

| my tracker on my note pad |

|---|

| selfie with my tracker on my note pad |

|---|

What are the unnecessary expenses that affect your income? Explain. |

|---|

There are some unnecessary expenses that may affect income if they are not checked. For me some of them the Includes;

Impulse Buying

Sometimes I see myself buy items that are not on my budget or that I didn’t plan for maybe because they looked attractive or are on sale especially the ones on sale because the prices are reduced.

Frequently Eating Out

I prepare meals at home but sometime I may be too tired to cook and I end up eating out or buying snacks and soft drinks or fast foods. These affects my income as it’s cheaper for me to cook at home.

Unplanned Transportation Costs

Transportation cost is rising by the day and sometimes I exceed my transportation budget due to hike in transportation costs and the transportation cost fluctuations by the commuters when there is hike in petroleum prices.

Excessive Data Consumption

Sometimes I spend more than budgeted on internet related usage due to the nature of my work and if my consumption usage is not monitored well.

These unnecessary expenses may appear small individually, but over time they consume a significant amount of income.

How do you save money from your income that will sustain you for future hardships? |

|---|

To save money from my income to sustain me during future hardships, I practice intentional saving by setting aside a fixed percentage of my income every month.

My Saving Strategy

- I ensure to save at least 20% of every income received. This also includes free money I get from people once in a while.

- I try to maintain an emergency fund.

- I also invest part of my savings in assets that can appreciate over time example is real estate.

- I avoid touching my savings except for genuine emergencies cases.

- I ensure to save this money in systems that also pays daily interest on my savings. So I get additional earnings when I save.

For example:

If I earn ₦250,000 monthly:

- Emergency Fund: ₦30,000

- Investment Fund: ₦20,000

Total Savings = ₦50,000

This habit will help me to create a level of financial security incase of a difficult period such as sickness, or unexpected expenses.

Have you ever created a budget that would improve your financial situation? Show us practically how. |

|---|

Yes.

A few months ago, I found out that I was spending excessively on snacks, transportation, and unplanned purchases, so I had to create a budget to improve my financial status.

For example:

Before Budgeting

| Category | Amount (₦) |

|---|---|

| Feeding | 80,000 |

| Transportation | 35,000 |

| Impulse Purchases | 30,000 |

| Savings | 10,000 |

After Budgeting

| Category | Amount (₦) |

|---|---|

| Feeding | 60,000 |

| Transportation | 20,000 |

| Impulse Purchases | 10,000 |

| Savings | 50,000 |

The result

- My savings Increased from ₦10,000 to ₦50,000 monthly.

- I reduced unnecessary spending.

- Helped me to improved my financial discipline.

- I had more money available for investments and emergencies.

This practical budget adjustment helped to improve my financial situation practically.

What advice would you give to others for great budget planning? |

|---|

The advice I would give to others for effective budget planning is:

- Track Every Expense:

Small expenses easily go unnoticed so they should try and track every expenses even the smallest ones and record them too. - Differentiate Needs from Wants:

They should spend on their needs first before wants. Wants can always wait as needs should be priority. Place them on a scale of preference and importance to know the ones to solve first. - Save Before Spending:

Savings should be a compulsory part of our budget. My father taught me the 70:30 principles. 70% for needs and 30% for savings and investments. - Create Realistic Budgets:

They should have a spending limit that matches their income. It’s like cutting your coat according to your size. We should live within our means. - Review Your Budget Regularly:

We should always review our spendings to ensure it’s in line with our budget and then adjust accordingly. - Avoid Debt for Non-Essential Items:

We should avoid impulse buying and we mustn’t buy everything we want and then avoid borrowing. - Invest for the Future:

We should learn to save and then invest our savings as it will help our money grow over time. Saving is important. We shouldn’t save to spend but save to invest

In Conclusion budget planning has helped me become more financially disciplined and prepared for cases of emergencies. Tracking my expenses, avoiding unnecessary spending, and saving a portion of my income, have helped me gained better control over my finances. I believe we all can improve our financial situation by developing and maintaining a simple and effective budget plan.

Here are my engagement links

link 1

link 2

I invite @oneray, @drhira and @mvchacin to join the challenge.

Leyendo tu publicación, vienen a mi mente algunas frases que he leído en libros y escuchado en audiolibros y podcast de crecimiento personal y financiero. Una de ellas es “No es cuánto ganas, sino cuánto puedes conservar de eso”.

Debo decir que muchas personas piensan que, la única manera de salir adelante es ganando más, pero, como bien lo dijo el autor de El hombre más rico de Babilonia en una de sus historias, la gente que no pone freno a sus deseos, tarde o temprano, gastará, aún, lo que no ha ahorrado, porque los deseos, al cumplirse el primero, inmediatamente aparece otro más grande.

Tus ejemplos son fantásticos. Y, como bien dices, no es que, después de gastar ahorro algo de lo que me queda; es pagarnos primero un porcentaje previamente asignado (en mi caso guardo más del 50 % de mis ingresos), y esto ha hecho que mi vida económica sea más sólida a través del tiempo.

Por otra parte, el agujero más pequeño puede llegar a hundir al barco más grande si no se encuentra y tapa a tiempo; así mismo son los gastos casi invisibles, que, por parecer pequeños, muchas veces no se consideran importantes.

Tomar decisiones conscientes es lo que más importa a la hora de gastar lo que nos queda, porque es una manera de autodemostrarse que hay una buena administración. Al final, nosotros somos simplemente administradores de los dones y el dinero que Dios pone bajo nuestro control.

Thoughtful response you have here freind. Saving 50% of your income is really a lot and requires alot of discipline . It’s good to know that you it has helped you in your financial journey. Thanks for stopping by and for your meaningful contribution.

Congratulations your comment support by team @steemcurator08 ,@sualeha

Greetings

Hello ma'am through your article I've learnt a lot about budgeting. I have been looking for ways to save most of my income but impulse buying would not let me but now I'm aware of how to avoid it through your Article. Thank you for sharing.

You are welcome sis

My X link

https://x.com/alexanderpeace4/status/2062257767038042243?s=46

Curated by: @ahsansharif

Thank you @ahsansharif for your support

Your thinking about budget is very good, you believe in saving and investing in the budget and you give more importance to these two while preparing the budget. I also believe that the steps you have taken are very effective, because saving is wealth, we should prepare the budget by keeping the wealth in order. I hope you will be able to implement your budget successfully and will be able to reach the peak of progress. I wish you success.