SLC32-W2 || Real Life Problem Solving Challenge: Budget Planning

As you said in your contest post, we need a proper budget to live a happy life without facing financial problems or lean patches by planning properly, whatever our earnings. As a corporate marketing professional posted in different countries, I earned a lot of money during my service period. I am still earning through project management and I don't deny I have also spent on unnecessary expenses, even if poor planning was never my problem.

I have never faced financial problems so I will explain how to improve our real lives by managing and tracking our expenses wisely. I am willing to participate and share my savings methods, personal budgeting experiences, and how I manage my weekly, monthly and long-term expenses.

Now I will answer your questions

How do you plan your weekly or monthly budget? Explain well.

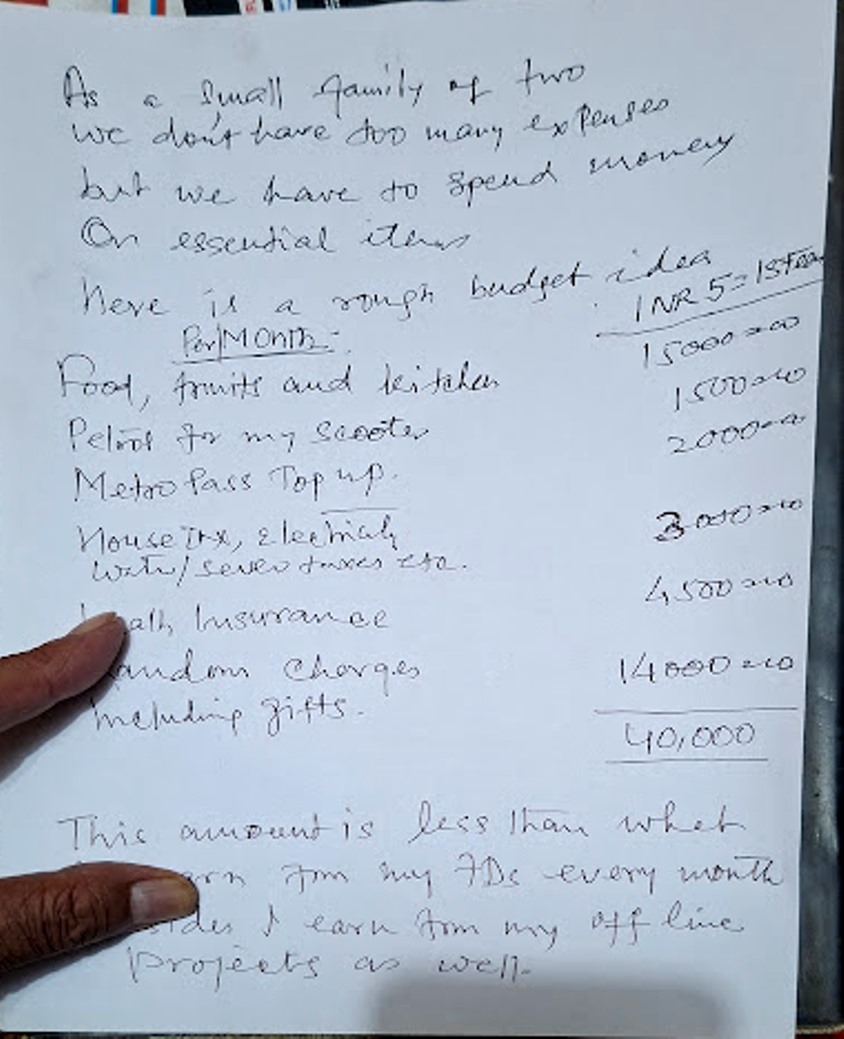

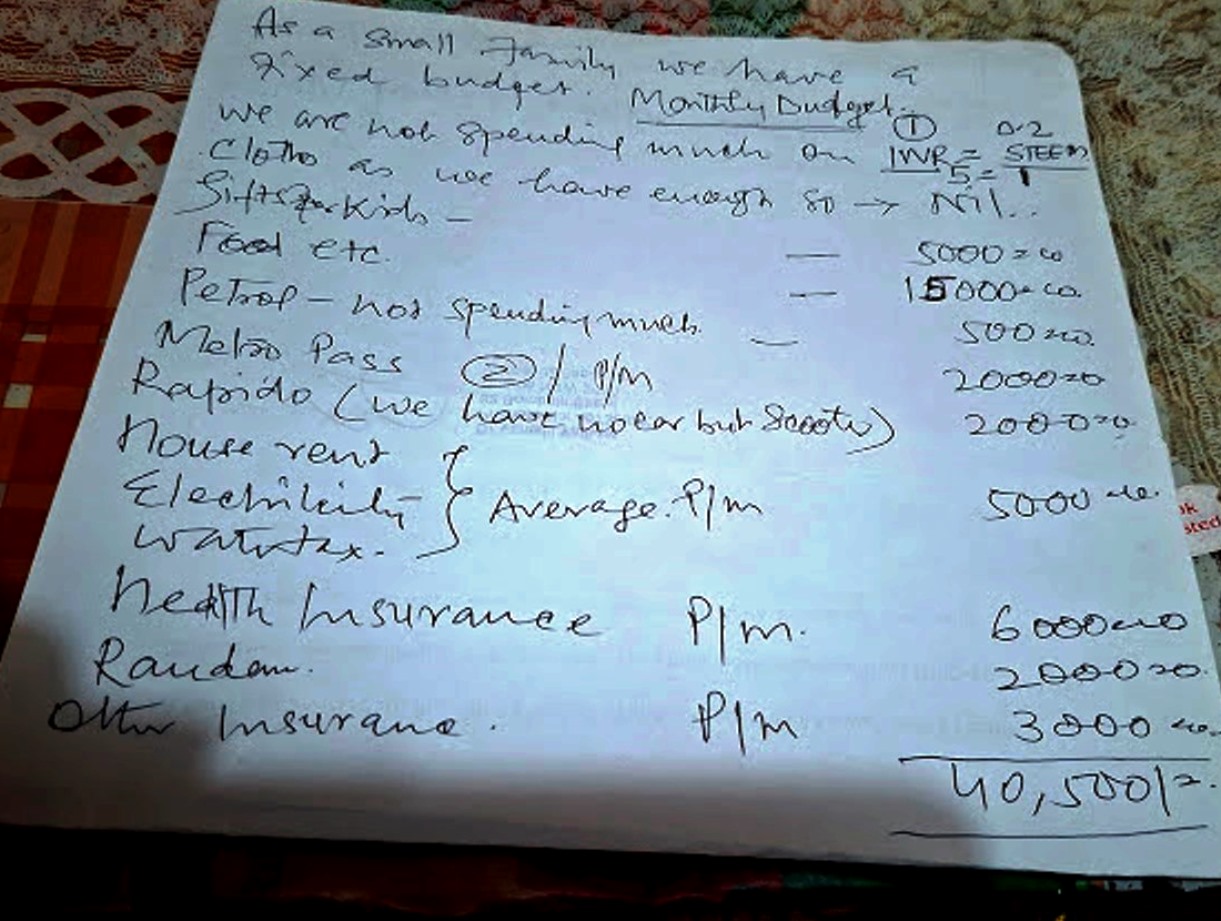

I suggest that to plan our budget, we need to know our priorities. So the first thing is to know our net income. As far as I am concerned, my tax was deducted at source, so all I had to do was keep a rough estimate of all my expected expenses.

For instance: fees for my daughter's education, kitchen, personal travel, insurance and other fixed bills like electricity, house tax, communication, water, etc., which included a column for unforeseen expenses.

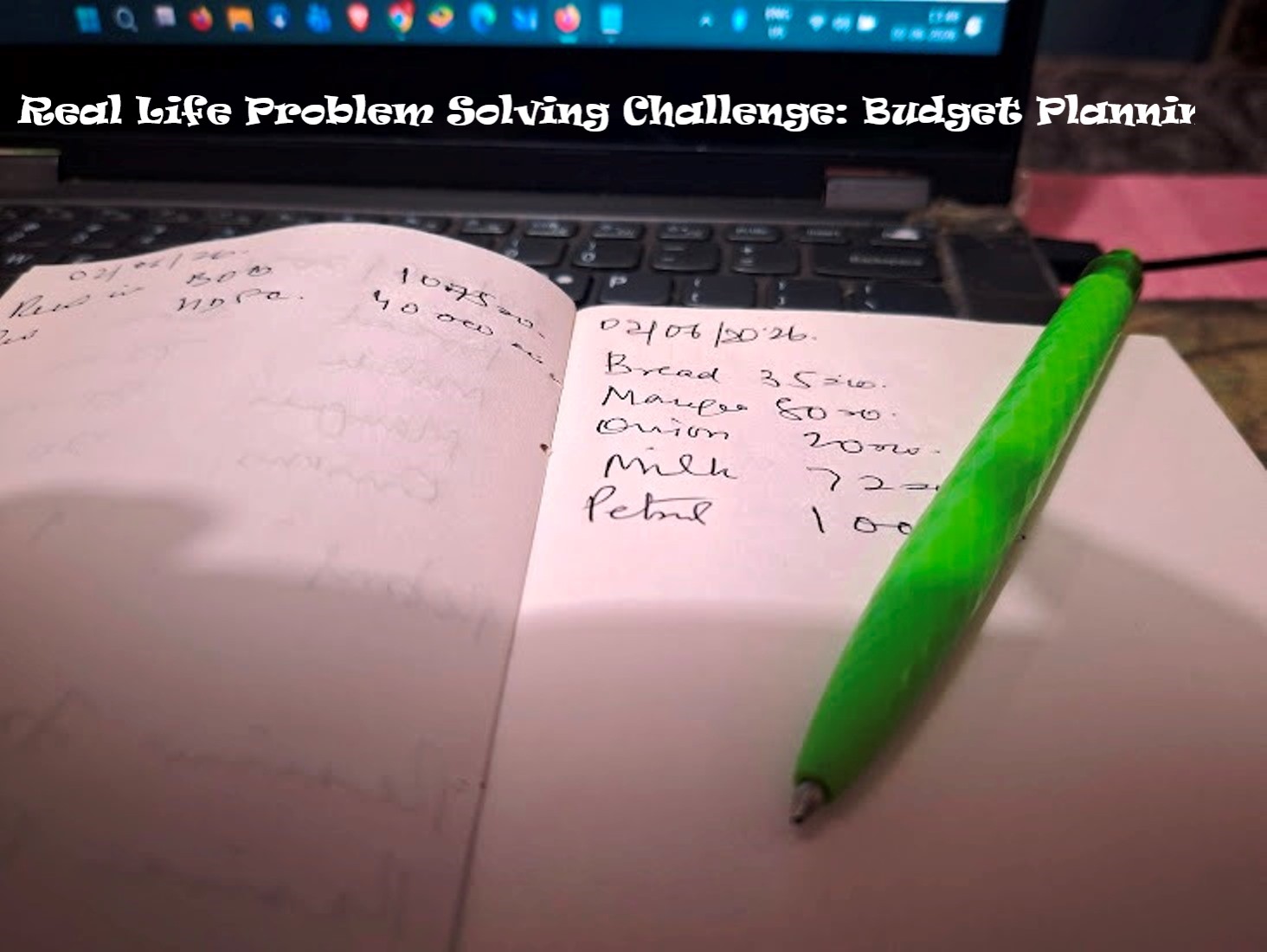

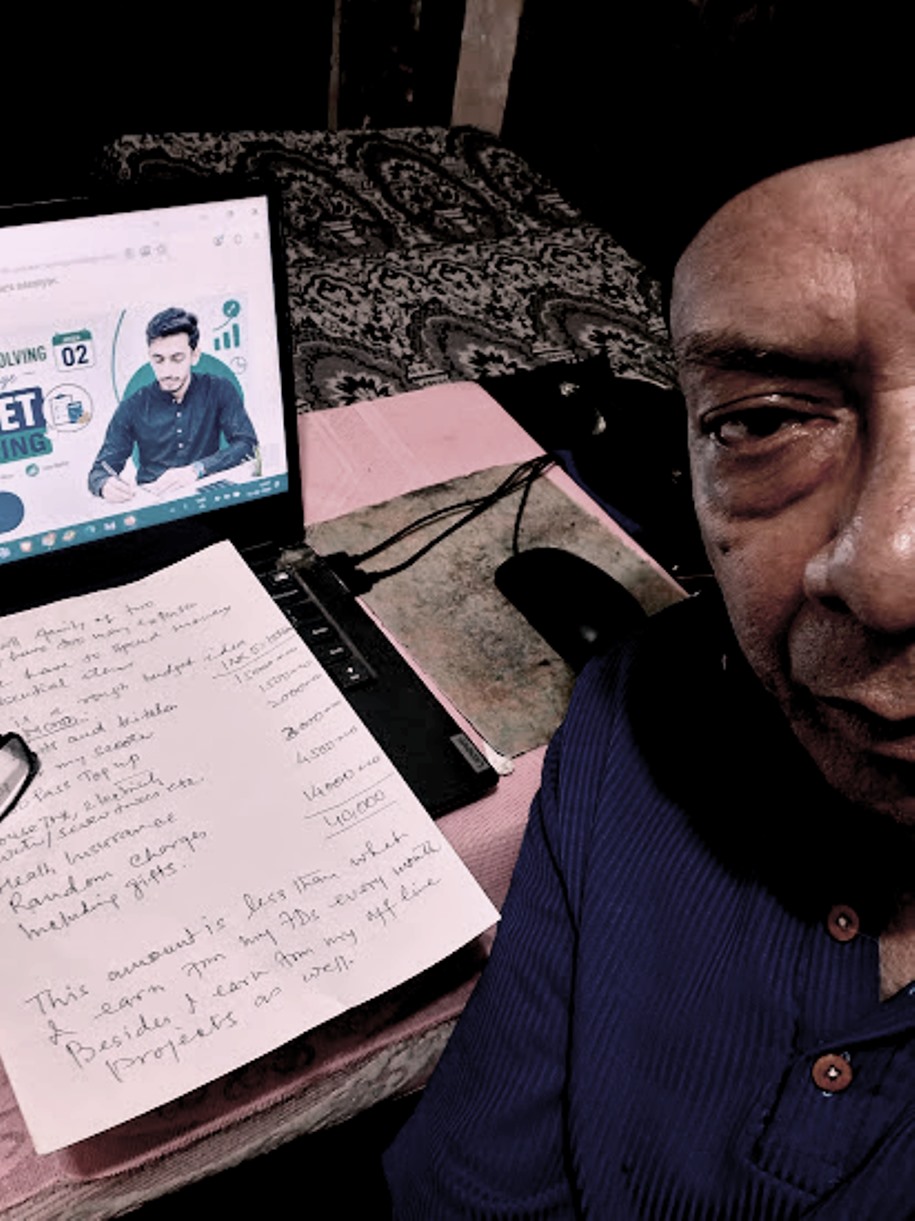

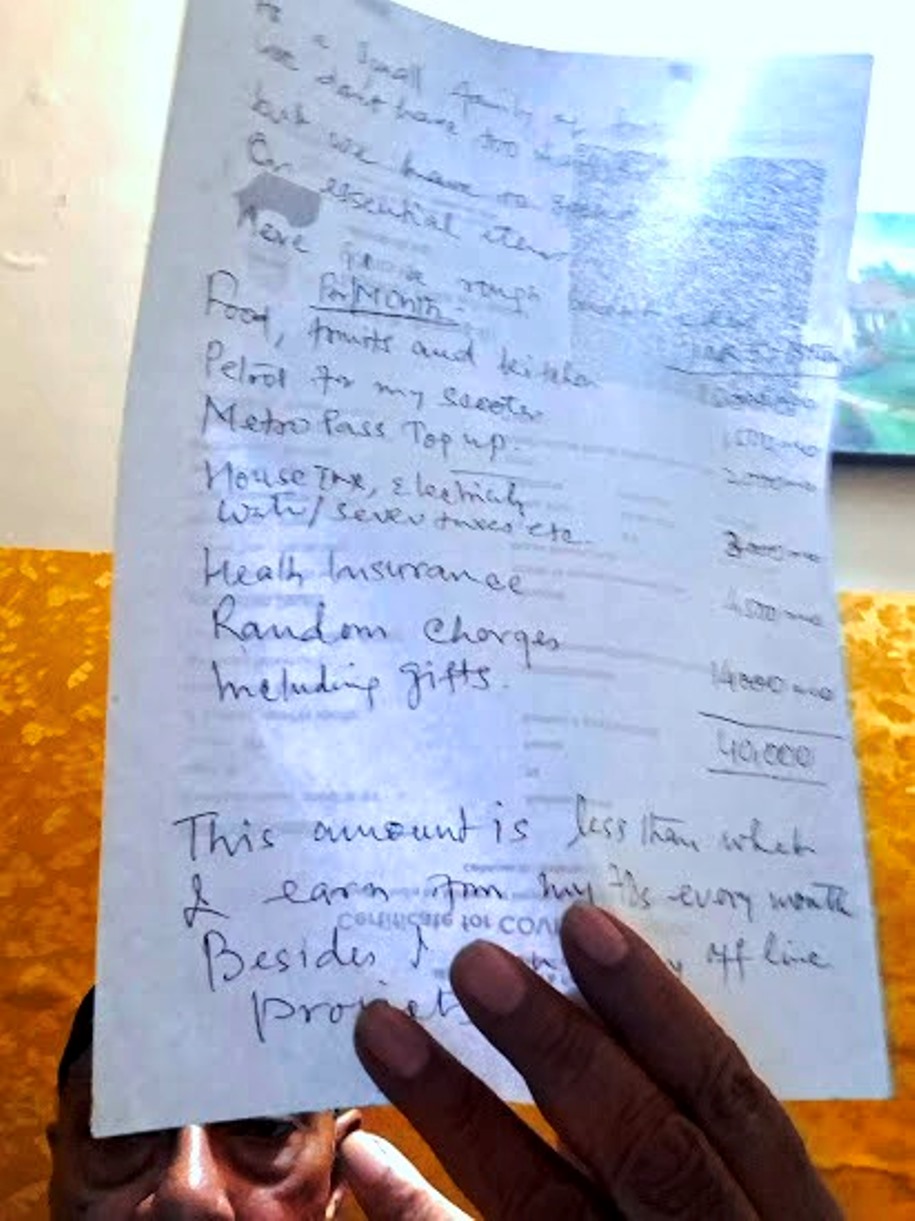

What tool or method do you use to track your expenses? Show at least one tool or method in detail with a selfie.

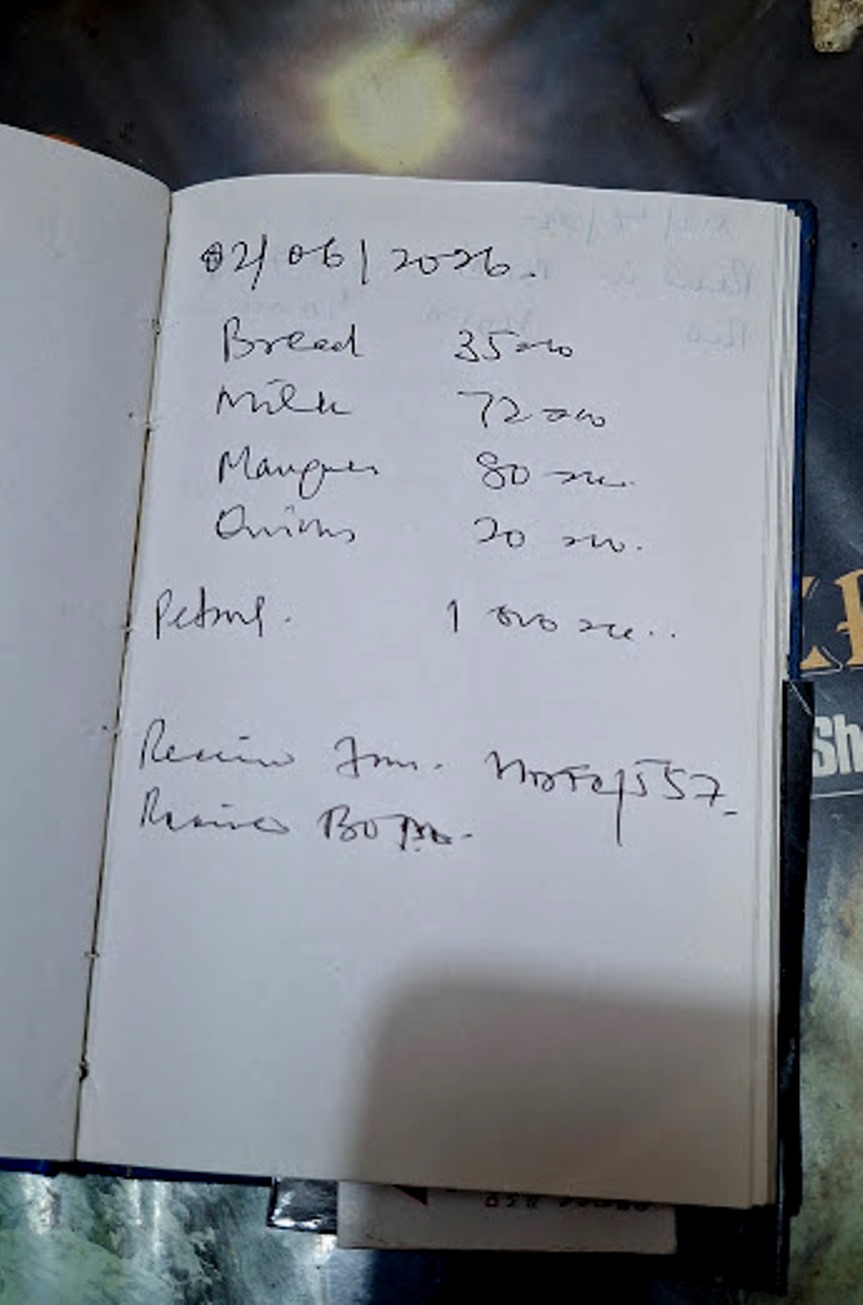

You will be surprised to know when I started my job there were no computers or mobile phones, so a simple domestic tool was my notebook-based expense register. We used to keep a diary which was our sole tool that kept all our records of income and expenses.

Would you believe that a small diary only for all expenses had a daily page for each day and included what we bought, what the washerman took for washing and ironing and what he brought back. My wife kept all the details including milk, vegetables and grocery as she noted every expense of the day.

Her method was simple: she would note down every expense on the date, item-wise, including my cigarettes (yes I used to smoke until 2004, which I gave up on her insistence). She never missed any expense on anything including food, travel, bills or others.

She noted down all expenses every day or even multiple times a day as and when she had time. You know I know many families which did the same and bought a diary or register every year to write all their spending immediately.

She would total the amount at the end of the day and open a new page the next day. That sure helped plan our budget. It might sound funny but I used to see a mark “unnecessary” X whenever she noted my cigarette expenses which I never told her the exact amount.

I appreciate her effort with writing every expense by hand daily, even small ones like tea or snacks or even cigarettes, and if a guest chewed paan she would note that too.

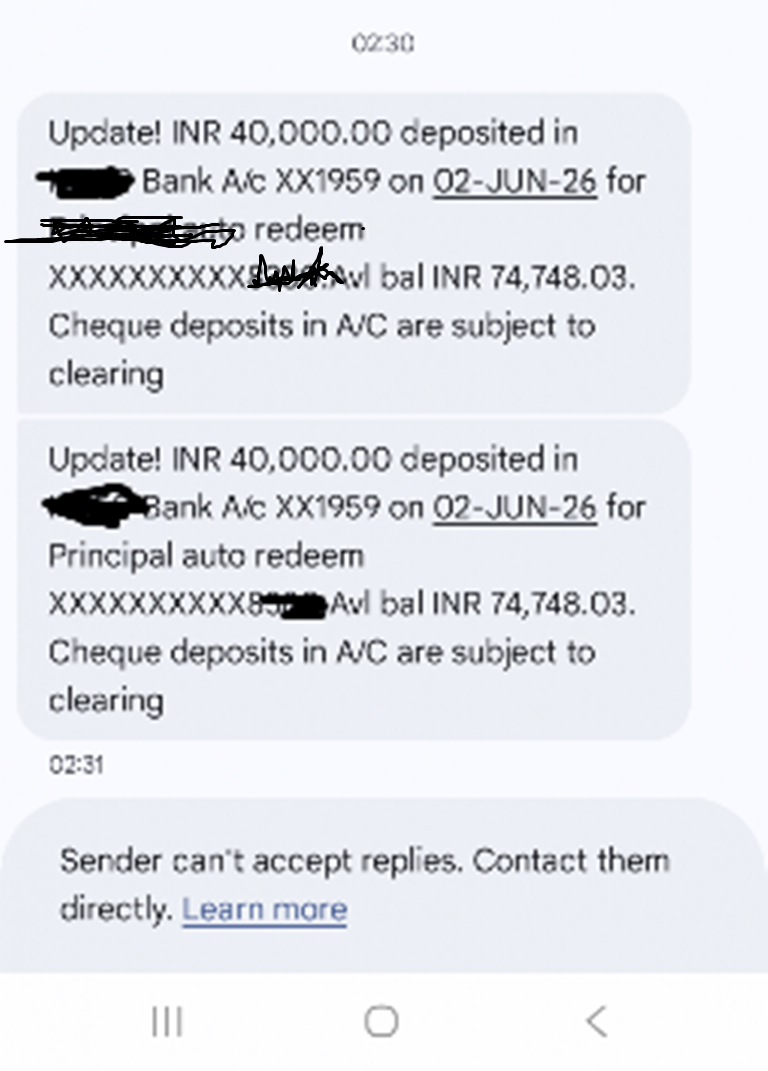

Today we have a number of such tools like Moneyview and other Indian apps which you can even link to your SMS or bank accounts to read transactions, set monthly budgets, or to see where money is going and coming from. Yes, I get messages of all spending or earning online but that gets registered in the associated account.

Oh, there is so much to learn and do nowadays but we are beyond that as I never bought anything on EMIs or left unpaid bills, so you see I utilized my earnings in full without getting worried about overspending. I am still doing the same minus diary writing.

What are the unnecessary expenses that affect your income? Explain.

This is a tricky question because I believe there are no unnecessary expenses unless you are a buyer who goes on impulse. As far as I am concerned, my expenses are mainly discretionary because these are chosen wants. If you spend on impulse that will slowly reduce your worth.

True, I was eating out frequently but I was paid for that by the company, so I never faced a problem like many do. I seldom ordered online when at home because I trusted sitting at the dining table and enjoyed homemade food since I was out most of the time on my marketing travels.

I believe today's generation is spending too much on outside food which is a perfect leakage in your income. Let me add I have not subscribed to different streaming services or been a member of a gym because even being a fitness freak I never pumped iron but relied on outdoor exercise.

I feel these might look like small expenses to many but they all cost you in the end. I feel surprised when I see people buying unnecessary gadgets without even knowing their use and buying clothes which they seldom use. I am sure this is the main problem most people face regarding their budget.

How do you save money from your income that will sustain you for future hardships?

A good thing was my father taught me a 70/30 formula which said whatever the condition, my expenses should not exceed more than 70% of my salary and the rest should go into a fixed saving plan, as you never know when you might face a rainy day.

Fortunately, I still had enough surplus even after all our expenses. To be frank I never trusted non‑essential spending, although going to a movie or eating out, shopping, buying things for the three of us occasionally was not outside our plan.

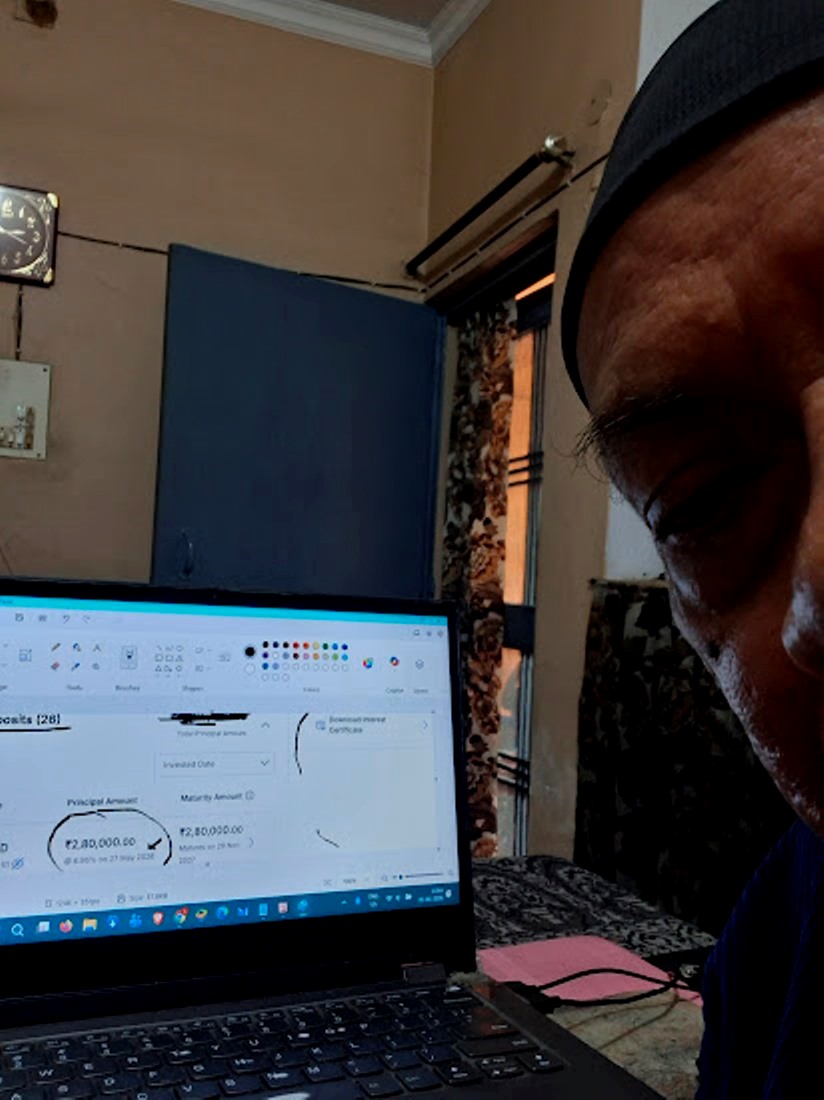

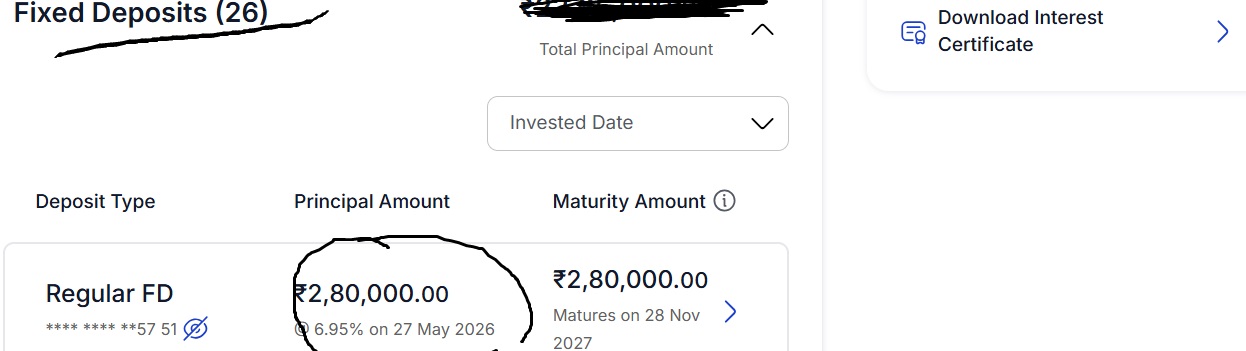

I have 37 FDs in my three different banks which mature quarterly as per my instruction and even the interest is more than enough for our survival.

So the best thing that happened to us was my father's advice because during my early service days our post office schemes were doubling all our savings in five years. I would buy post office saving certificates every month and kept doing that for twenty years even if the interest rates were reduced in later years. You will be surprised to note that at the end of 20 years my interest return was almost equal to my monthly salary.

The last one I renewed on 27th May in one of my three banks.

Have you ever created a budget that would improve your financial situation? Show us practically how.

Let me accept that creating a budget actually improves your financial situation if you write your net income, list fixed needs like all your essential expenses depending on your family needs, and finally subtract it all from your income.

I also suggest saving a fixed amount regularly that you can afford easily, but that should be a compulsory habit. You might want to spend the remaining amount for eating out and shopping, but wait and think—is that necessary?

Although we have well passed the age of creating budget we keep a tab

Finally keep a close watch on all your expenses and in case you see yourself going overboard, cut unnecessary spending. In the end, everyone knows better about their income, family and future plans so I suggest you do what you feel is best in your circumstances.

What advice would you give to others for great budget planning?

As they say every penny is worth saving but can you do that? No, that's not practical.

Then I could have suggested the standard saying what everyone keeps suggesting to follow "50% needs, 20% savings, 30% wants and stick to it." But that is bookish and I am not telling you that.

- My first suggestion save enough so you get a fixed income even if you have no job

I suggest you to keep your expenses under control, save enough for rainy days, keep inflation in mind and follow a patterns for saving early or should I say right from when you start earning.

I had a rule that I followed during my regular job, or my retainer ship days when I was working on project basis and even today when I am no more in a job but still following the rules as my earnings have not gone down, yet I can still save from my current earnings.

I still keep a strict watch on my expenses even if I have no liabilities or responsibilities. Would you believe that I have not spent a single Steem for my personal use even if I withdrawn a couple of thousand but using them for investment in crypto market.

In the end, I don't believe in spending just because I have money to spend and it's the same when I say I don't give bookish suggestions but believe in practical ones, so do what suits you best.

I invite @sualeha, @ruthjoe and @suboohi to join this contest by @ahsansharif

Establishing our priorities is a key ingredient for effective budget planning, this is because we all have different needs and view satisfaction diffrentĺy.

I also noticed that your wife works as your auditor, keeping your expenses under check, and a Dad who taught you the 70/30 rule. You surrounded yourself with people who were a plus to your growth.

Thanks, yes she did all the hard work for saving as much as possible.

Congratulations, your comment has been upvoted by the Steemcurator08 team. Keep up the valuable comments.

***Curated By: @sojib1996 ***

Hola @dove11

Ha sido muy interesante leer tu publicación. Me gustó especialmente cómo compartiste tu experiencia personal y la importancia que ha tenido la disciplina financiera a lo largo de tu vida. Sin duda, llevar un control de los gastos y manteer el hábito del ahorro son prácticas que pueden marcar una gran diferencia en nuestro futro.

Me pareció muy valioso el consejo que recibiste de tu padre sobre la regla del 70/30. Es una estrategia sencilla pero efectiva para garantizar que siempre exista una reserva para afrontar imprevistos y alcanzar metas a largo plazo. También fue inspirador conocer cómo tu familia utilizaba un diario para registrar cada gasto diario, demostrando que la organización y la constancia son herramientas poderosas para una buena planificación presupuestaria.

Gracias por compartir consejos tan prácticos y experiencias reales que pueden servir de inspiración a muchas personas que desean mejorar su situación financiera. Te felicito por tu dedicación y por mostrarnos que el ahorro y la planificación son hábitos que ofrecen tranquilidad y estabilidad con el paso de los años.

Te deseo mucho éxito en este desafío.

Saludos y bendiciones.

Thank you so much, but the fact is even if a person completes a first cycle of say as in my case it was 5 years to double the money. I deposited a fixed amount every month for 5 years and then renewed it every month on maturity for 25, my amount became 16 times which is still giving me enough interest. So I only had to deposit for five years but in my case I increased the basic amount on every maturity.

https://x.com/dv11_s/status/2061831628167729510?s=20

High-Yield Curation by @steem-seven

Your content has been supported!

Maximize your passive income!

Delegate your SP to us and earn high rewards

Click here to see our Tiered Reward System

We are the hope!

Budget planning is very important and helpful to us. I like your budget planning and I have pick some of your advice.