Quantitative Finance on TRON: Building and Backtesting a Mean Reversion Strategy

The cryptocurrency market operates 24/7, making it an ideal environment for quantitative trading strategies. Rather than relying on emotions or news alone, quantitative finance uses mathematical models and statistical analysis to identify trading opportunities.

In this article, we'll build a simple Mean Reversion strategy that anyone can test on historical TRON (TRX) price data.

Why Mean Reversion?

Financial markets often experience short periods where prices move excessively away from their average. A mean reversion strategy assumes that these deviations eventually return toward the mean.

The basic idea is simple:

Buy when the price is significantly below its recent average.

Sell when the price rises significantly above it.

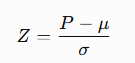

One common statistical tool for measuring this deviation is the Z-Score.

Where:

P = Current Price

μ = Rolling Moving Average

σ = Rolling Standard Deviation

Trading Rules

Z < -2 → Buy

Z > 2 → Sell

Otherwise → Hold

Why This Matters

Unlike random trading signals, quantitative strategies can be:

Backtested

Optimized

Measured objectively

Automated

The goal isn't predicting the future—it's determining whether an idea has demonstrated a historical statistical edge.

Python Backtest Example

Below is a complete example that you can run yourself.

import yfinance as yf

import pandas as pd

import numpy as np

Download TRON historical data

data = yf.download("TRX-USD", start="2022-01-01")

Rolling statistics

window = 20

data["MA"] = data["Close"].rolling(window).mean()

data["STD"] = data["Close"].rolling(window).std()

Z-Score

data["Z"] = (data["Close"] - data["MA"]) / data["STD"]

Trading Signals

data["Signal"] = 0

data.loc[data["Z"] < -2, "Signal"] = 1

data.loc[data["Z"] > 2, "Signal"] = -1

Daily Returns

data["Returns"] = data["Close"].pct_change()

Strategy Returns

data["Strategy"] = data["Signal"].shift(1) * data["Returns"]

Cumulative Performance

data["Market"] = (1 + data["Returns"]).cumprod()

data["Strategy Equity"] = (1 + data["Strategy"]).cumprod()

print(data[["Close","Z","Signal"]].tail())

print(f"Market Return: {(data['Market'].iloc[-1]-1)100:.2f}%")

print(f"Strategy Return: {(data['Strategy Equity'].iloc[-1]-1)100:.2f}%")

Possible Improvements

Professional quantitative funds rarely stop at a single indicator.

Some ideas to improve this model include:

Volatility filtering

ATR-based stop losses

Position sizing using Kelly Criterion

Bayesian parameter optimization

Cointegration and statistical arbitrage

Regime detection using Hidden Markov Models

Machine Learning feature engineering

Walk-forward optimization

Monte Carlo robustness testing

Key Performance Metrics

When evaluating any trading strategy, total profit alone isn't enough.

Professional quants typically analyze:

Annualized Return

Sharpe Ratio

Sortino Ratio

Maximum Drawdown

Calmar Ratio

Win Rate

Profit Factor

Average Trade Duration

A strategy with lower returns but significantly lower drawdowns may actually be superior from a risk-adjusted perspective.

Final Thoughts

Quantitative finance transforms trading from guesswork into a process driven by data, statistics, and repeatable rules. While no strategy is guaranteed to remain profitable, rigorous backtesting and risk management can help identify approaches worth exploring.

This simple mean reversion model is just a starting point. As you gain experience, you can combine statistical signals, machine learning, and blockchain-specific metrics to create more sophisticated systems.

Have you ever backtested a strategy on TRON or another cryptocurrency? I'd be interested to hear what techniques or indicators you've found most effective.