Cross-Border Payment Cost Analysis: Wires, Money Transfer Services, and Crypto Cards

A useful comparison framework for fintech evaluators

For operators, corporate buyers, and individual users evaluating cross-border payment options, the cost comparison across categories has shifted meaningfully. Crypto-funded cards have moved from niche option to legitimate competitor for specific use cases, and the analysis now needs to include them as a real category. This walks through the actual cost structures at typical individual transaction sizes and which use cases each category fits.

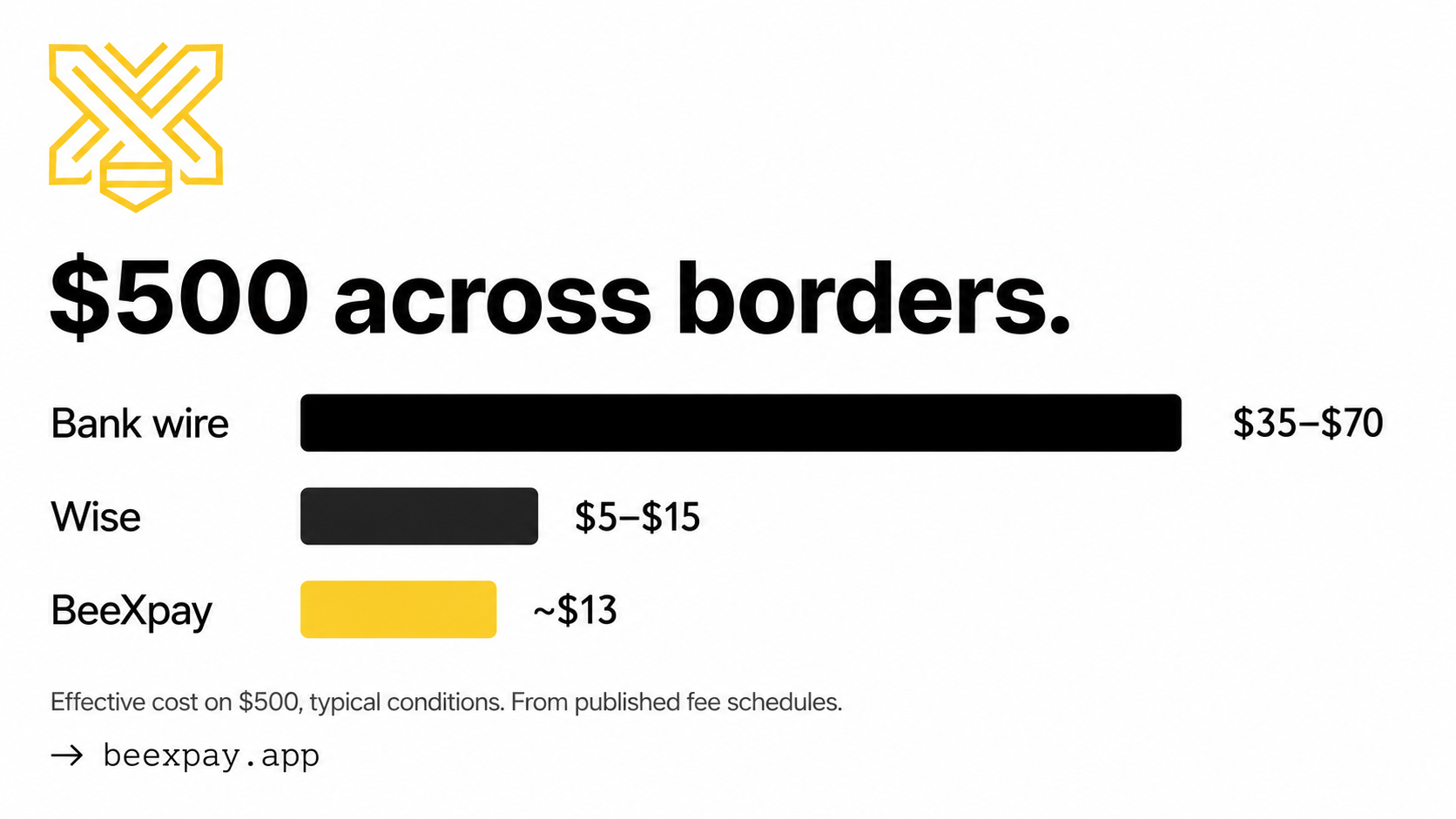

Bank wires: cost structure and use case fit

The $25–$50 flat fee plus 2–4% FX spread reflects infrastructure designed for high-value, low-volume institutional transfers. At $500, effective rates run 7–14% including intermediate bank fees. At $5,000, the rate compresses to around 4%. Bank wires fit large infrequent transfers and situations requiring traditional banking documentation. They don't fit recurring small cross-border transactions.

Money transfer services: middle of the spectrum

Wise: 0.5–1.5% effective on common pairs. Western Union and MoneyGram: 4–8% with cash pickup. PayPal cross-border: 2–4%. These fit recipient-focused transfers where the goal is delivering money to someone abroad. They compete on user experience and FX transparency rather than just cost.

Crypto cards: the structural alternative

BeeXpay with Full KYC: 2.5% reload + flat $0.25–$0.50 + 1.5–2% bank FX on non-USD. For $500 funded and spent across 10 transactions averaging $50: $16–$26 total, 3.2–5.2% effective. The model competes on workflow integration with crypto holdings and on cost for distributed online spending.

Use case mapping

Large lump-sum: bank wires for regulatory clarity, Wise for cost. Recipient-focused: Wise or Western Union depending on cash pickup. Distributed online cross-border spending: crypto cards become competitive. Personal travel: physical crypto card or international debit card by volume. Categories optimize for different patterns; choice should follow pattern.

What corporate buyers should consider

For corporate buyers evaluating cross-border infrastructure for distributed teams or contractors, the crypto card category opens use cases that lacked good answers before. Contractor payments where local banking is weak. Small recurring vendor payments. Geographic flexibility for expense management. Not a replacement for all infrastructure, but it fills gaps traditional options handle poorly. Pilot programs on specific use cases provide better evidence than marketing comparisons.

Implications for fintech category strategy

Crypto cards competing legitimately on cost with money transfer services represents a meaningful development. For incumbents, the cost moat has narrowed; differentiation needs to come from experience, recipient coverage, regulatory clarity. For challengers, the category is established enough to compete on workflow integration rather than novelty.

Honest limits

The card model doesn't win universally. Geographic restrictions apply (US, UK, Russia, others). It requires crypto holdings or willingness to acquire them. Heavy local-currency in-person spending raises effective costs. Very small infrequent transactions may not justify the workflow learning curve.

Closing observation

The interesting development in cross-border payments in 2026 is not the existence of crypto-funded options but their evolution into legitimate cost competitors for specific use cases. Worth understanding category-by-category rather than dismissing or championing as a whole.

→ Try it: https://beexpay.app