Low-Commitment Evaluation in Fintech: The $10 Virtual Card Entry Point

The evaluation problem in newer fintech categories

For fintech products in established categories — current accounts, credit cards, savings products — comparison-based evaluation works reasonably well. Users have prior experience with similar products and can compare features, fees, and reputation meaningfully. For products in newer categories — crypto cards, on-chain payment instruments, hybrid fintech-crypto products — comparison provides less signal because the products do something the user hasn't experienced before. Whether the workflow actually fits a given user depends on specific circumstances (income source, spending pattern, geography, current alternatives) that no general description can capture accurately. The result is evaluation friction that limits category adoption even when individual products would fit individual users well.

Why low-cost trial is the structural answer

The answer to this evaluation problem isn't better marketing or more reviews — it's reducing the cost of trial to the point that users evaluate based on their own use rather than on indirect information. For payment products specifically, this means: low entry cost, immediate ability to use the product on real transactions, easy walk-away path, and smooth upgrade path if the trial succeeds. Each element matters. Low entry cost means users will actually try rather than continue researching. Real-transaction usability means the trial reveals real friction rather than simulated friction. Easy walk-away means users don't feel committed during evaluation. Smooth upgrade means good trials translate to adoption without re-evaluation.

The economics of trial design

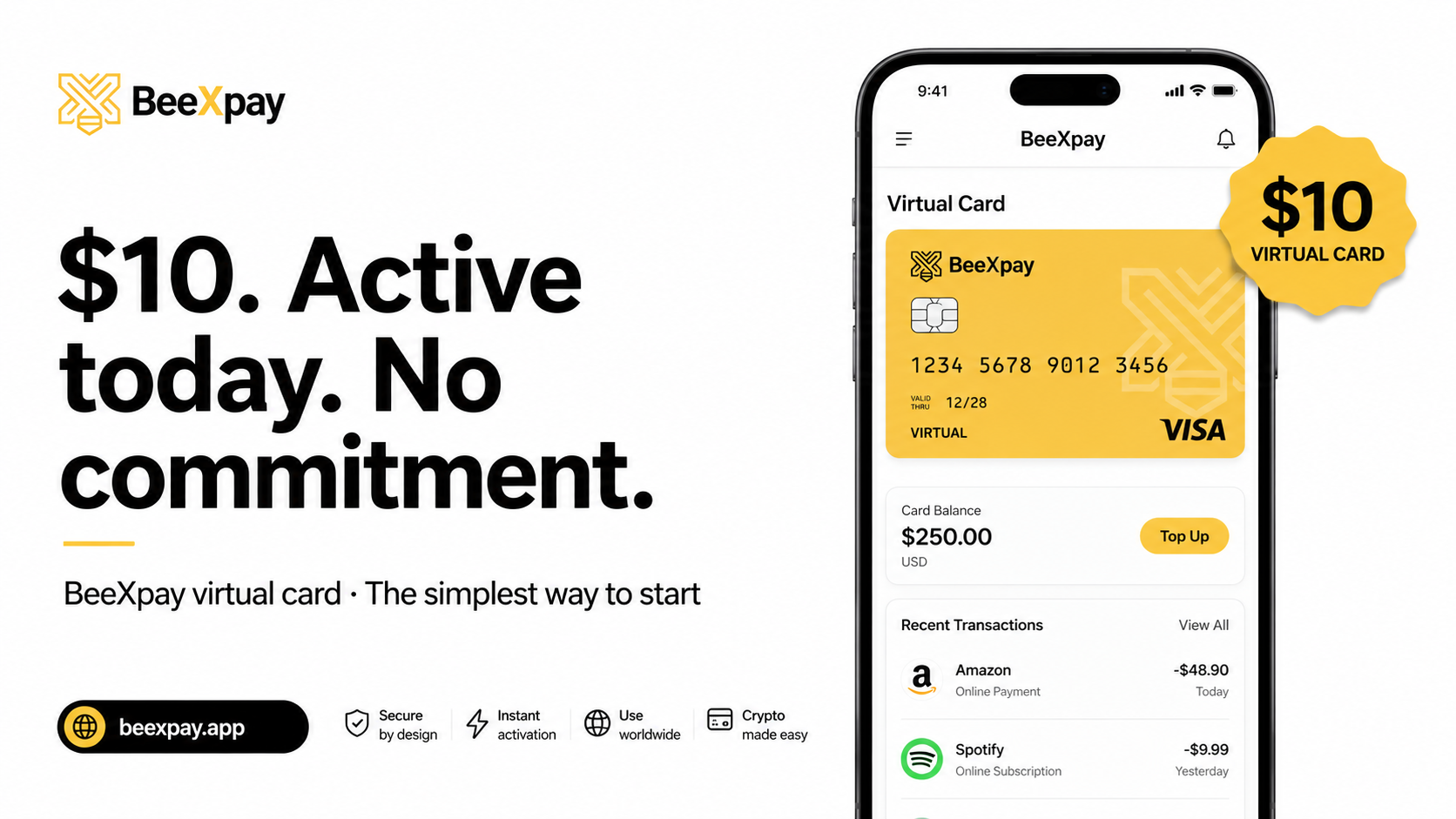

For an operator, designing for low-commitment trial has implications. The unit economics need to support customers who try and don't adopt, which means trial-tier pricing has to cover the operational cost of brief usage without depending on retention. The upgrade conversion rate from trial to full tier matters more than first-touch acquisition. The user experience during the trial has to be aligned with what full users would experience, not a degraded preview, or the trial doesn't reveal whether the full product fits. BeeXpay's design — $10 virtual card with Light KYC via Telegram, full functional capability for online spending, 4% reload versus 2.5% at Full KYC — fits this pattern: the trial tier is a real version of the product, just with slightly higher fees that reflect the lighter verification.

What the trial actually reveals

A useful trial generates specific information about the user's fit. Time from funding to spendable balance (varies with crypto network choice). Whether the card works at the user's intended merchants (particularly important for users in regions with BIN issues on local cards). How the workflow feels relative to the user's current alternatives. Whether the fee structure on actual transactions matches the published structure. How the Telegram interface fits the user's preferences for routine operations. Each of these has a concrete answer that emerges only through actual use. The information value of this answer set is significantly higher than the dollar cost of generating it.

When the trial reveals adoption-worthy fit

Adoption-worthy fit usually shows up through specific signals during a trial: the workflow feels simpler than what the user was doing before, the fees match expectations on the user's actual transaction sizes, the card works at the intended merchants, the interface is intuitive enough for routine use. When these signals appear, the user has the information to support an upgrade decision — typically Full KYC for the better economics, possibly a physical card for in-person spending. The smooth in-app upgrade path matters here because users who'd face re-evaluation friction often don't complete the adoption step even after a successful trial.

When the trial reveals poor fit

Poor fit also reveals itself clearly. High effective fees relative to transaction size (typical for small-transaction-dominant patterns). Friction acquiring crypto for funding (typical for users without existing crypto holdings). Merchant blocks beyond BIN screening (typical for some merchant categories or geographies). Workflow complexity relative to alternatives (typical when alternatives are already well-suited to the user). When these signals appear, the trial has done its job: the user has confirmed that this specific product doesn't fit their specific situation, and they can stop using it without ongoing cost. The trial cost is the price of learning this with certainty rather than guessing.

Implications for fintech product strategy

For fintech operators in newer categories, the lesson is that low-commitment trial design is not optional — it's the structural answer to category-specific evaluation friction. Products that require high commitment to try will be researched extensively and adopted slowly. Products that can be tried cheaply will be evaluated by users who would never have completed extensive research but might complete a $10 trial. The conversion economics depend on the product actually fitting users who try, which loops back to product-market fit at the granular level: which specific user populations does the product fit, and is the trial design structured to let those populations find out cheaply? For BeeXpay specifically, the virtual card via Telegram fits this strategy by design — it's not a marketing variant of the product, it's the version of the product structured for evaluation.

Closing CTA

For category-level fintech adoption, low-commitment trial design addresses an evaluation friction problem that feature marketing can't solve. The $10 virtual card via Telegram is a worked example.

Start the trial → https://t.me/Beexpay_bot