USDT vs USDC: How the Stablecoin Choice Affects Your Crypto Card Funding

The question that comes up after the first deposit

A user opens their BeeXpay account, decides to fund the virtual card, and reaches the deposit screen asking them to pick a stablecoin and network. They've heard of USDT and USDC but aren't sure which to pick or whether it matters. This article walks through the practical differences without ideological framing or speculation about which is winning.

Functional similarity: both work, both peg to USD

Both peg to USD and aim for a 1:1 ratio. Both work for funding a BeeXpay card. Both convert to USD at the moment of card spending, in around five seconds. From a pure card-funding perspective, the two are functionally interchangeable. The differences emerge in surrounding context: liquidity, network costs, regulatory framework, and acquisition channels.

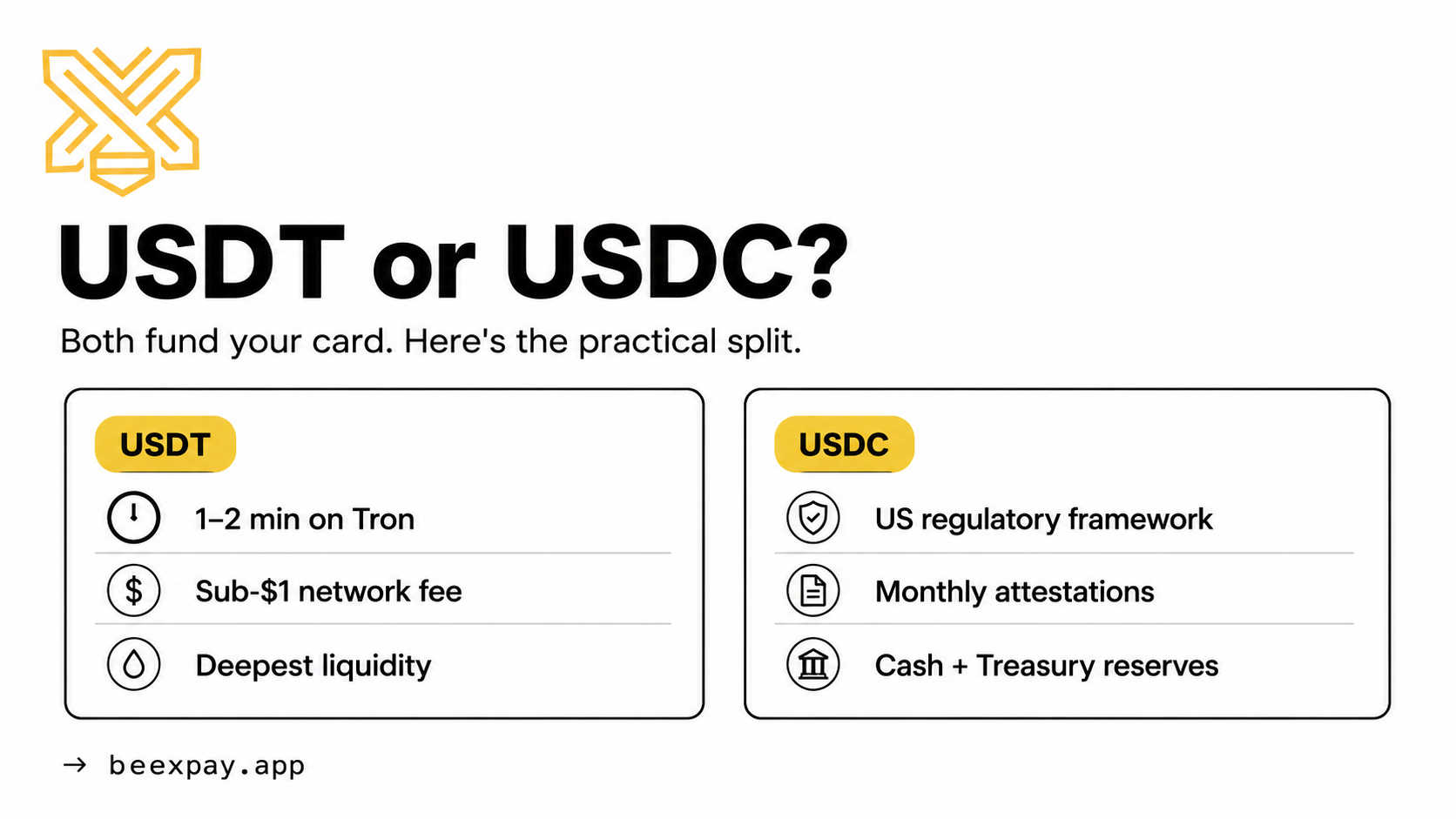

USDT: scale and reach

USDT is the largest stablecoin by market cap and trading volume. Listed on nearly every major exchange, accepted on virtually every P2P platform, available across more networks than any competitor. For users in markets without deep crypto infrastructure, USDT is often the only stablecoin available with consistent liquidity. In regions like Pakistan, India, Indonesia, Vietnam, parts of Africa, USDT is functionally the default because it's what's actually available at thin spreads.

USDC: regulatory framework and reserve transparency

USDC operates under stronger US regulatory framework, with monthly attestation reports and reserves held predominantly in cash and short-term US Treasury bills. The attestation cadence and reserve composition are more transparent than USDT's. For users who place high weight on regulatory backing — institutional users, employees of regulated companies, users in jurisdictions where stablecoin compliance is becoming explicit — USDC offers a structurally different risk profile. The trade-off is less liquidity in some markets and typically higher network fees, particularly on Ethereum.

Network costs: the variable that matters most for small amounts

For a user funding $50–$200, network fees can represent a significant portion of cost. USDT on Tron: $0.50–$1. USDC on Solana: $0.10–$0.50. USDC on Base: $0.20–$1. USDT on Ethereum: $3–$15. For small funding amounts, picking the right network for the stablecoin matters more than picking the stablecoin. The fee on a $50 funding ranges from 0.2% to 30% depending on network choice — a wider range than the difference between stablecoins on the same network.

Confirmation speed

USDT on Tron: 1–2 minutes. USDC on Solana: seconds. USDC on Base: 1–2 minutes. Either on Ethereum: 5–10 minutes calm, longer during congestion. For same-day issuance or urgency topup, Tron USDT and Solana USDC are the fastest practical options. Both are reliable enough that the speed difference between them is rarely the deciding factor.

Acquisition channels in different markets

Where users acquire stablecoins varies by region. In the US: Coinbase, Kraken, Gemini offer easy USDC; USDT is more variable. In Europe: regulated exchanges favor USDC. In Asia and Middle East: Binance, Bybit, OKX, and local P2P offer broad USDT access; USDC available but less ubiquitous. In Pakistan, Indonesia, and similar markets: P2P channels for USDT are typically the most practical route. The right choice often defaults to whatever the user can conveniently acquire locally.

Reserve composition transparency

USDC publishes monthly attestation reports showing reserves in cash deposits and short-term US Treasuries. USDT publishes quarterly attestation reports with reserves spanning cash, equivalents, secured loans, corporate bonds, precious metals, and other holdings. The compositions differ, the transparency cadences differ, and individual users weight these differently. Neither is hidden; the question is which composition the user prefers.

What BeeXpay's flow looks like

BeeXpay's deposit flow accepts both stablecoins across major networks. The user selects source asset and network during deposit, sends funds, waits for confirmation, and the card balance updates. The platform handles conversion to USD at the moment of card spending. The stablecoin choice doesn't affect the card's behavior at merchants — once funded, USD is what gets spent.

Practical recommendation framework

For most users: USDT on Tron if you're in a market with deep USDT availability and prioritize speed and cost. USDC on Solana if you're in a regulated market and prioritize reserve transparency. The right answer depends more on what you hold and what's locally available than on absolute superiority. If you have both, USDT on Tron is typically fastest and cheapest. If you have one, use what you have — both work fine.

What this doesn't change

The funding choice doesn't change the card's behavior, fee structure, or merchant acceptance. BeeXpay's structure — $10 issuance, 4% reload (Light KYC) or 2.5% (Full KYC), $0.25–$0.50 flat per USD transaction, 1.5–2% bank FX on non-USD — applies identically regardless of funding source.

Discussion:

What drove your stablecoin choice — local availability, regulatory comfort, network cost, something else? Worth thinking about whether the choice is right for your situation or just a default inherited from how you first acquired crypto.

→ Try it: https://beexpay.app