Why Fee Transparency Matters as a Product Quality Signal

The category variance in fee disclosure

Fee disclosure in fintech varies widely. Some operators publish complete fee schedules in clear language. Others surface only headline rates in marketing and hide details in terms of service. Users evaluating products often focus on the headline rate and miss the layered fees that emerge in actual use. The level of fee transparency is a real signal about operator philosophy — operators with clean fee disclosure typically have clean operational practices generally.

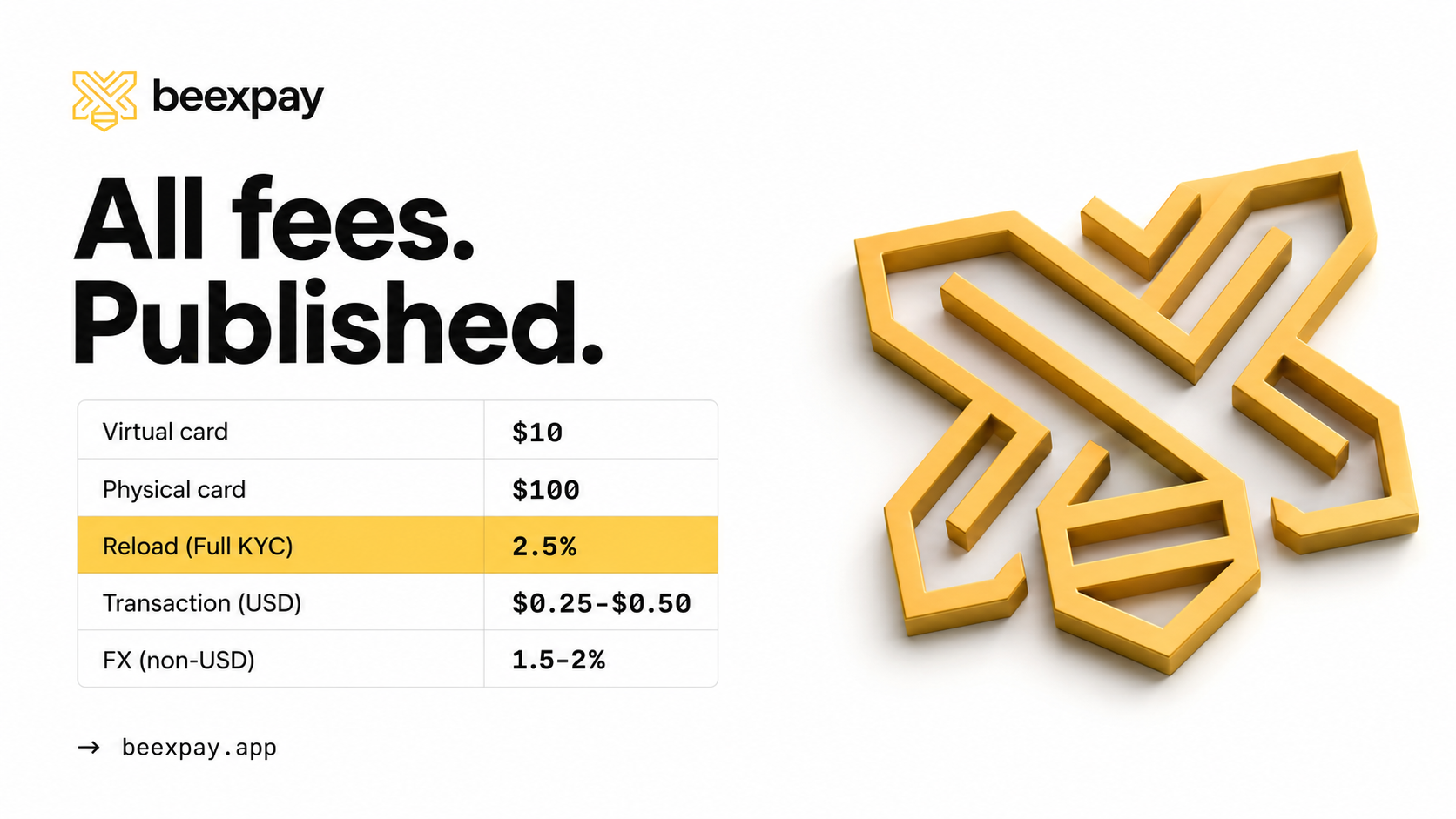

BeeXpay's published structure

Virtual card: $10 one-time issuance for Light KYC; included with Full KYC. Physical card: $100 one-time, Full KYC required, ~2 weeks delivery. Reload fee: 4% (Light KYC) or 2.5% (Full KYC) on funded amount. Per-transaction fee: $0.25-$0.50 flat for USD merchant transactions. Non-USD merchant transactions: 1.5-2% bank FX applied by the card network. KYC is free. The structure has limited categories — issuance, reload, transaction, FX — and each is documented.

What each fee covers

The reload fee covers crypto-to-USD conversion and operational overhead. Percentage-based on the funded amount, scaling linearly. The flat transaction fee covers card network costs and platform per-transaction handling. The non-USD FX is the bank network's USD-to-merchant-currency conversion fee, set by network rules rather than by BeeXpay. The pass-through framing matters because the FX is commonly misattributed to the issuer.

What's notably absent

Several common fee categories aren't in BeeXpay's structure. No monthly maintenance fees. No annual fees. No inactivity fees. No closure fees. No fees for freezing or unfreezing. No fees for viewing transaction history. These absences are notable because they're standard revenue lines for many providers. The structure is constrained in what it charges as well as comprehensive in what it documents.

Comparison to traditional bank cards

Traditional debit and credit cards often have foreign transaction fees (2-4%), ATM withdrawal fees ($3-$5 plus surcharges), monthly account fees, overdraft fees, statement fees, and other line items that don't appear in marketing. The fee experience for traditional cards often involves discovering fees through transactions rather than reading a published schedule. BeeXpay's structure is cleaner — fewer categories, all documented, all percentage or flat (no escalating structures).

Comparison to other crypto cards

The crypto card category has wider fee disclosure variance than traditional cards. Some operators publish detailed schedules; others surface only headline rates. Some charge per-transaction percentages of 3-5% versus BeeXpay's flat fee. Some have monthly minimums or maintenance fees. BeeXpay's published structure is on the simpler and more transparent end of the category, though this varies across operators — the category isn't uniform on fee transparency.

Modeling monthly costs

The math for typical monthly costs is straightforward. Annual issuance: $10 per virtual or $100 per physical (one-time). Monthly reload: percentage × monthly spending. Monthly transaction: ~$0.35 × number of transactions. FX: 1.5-2% × non-USD spending. For $1,000/month USD-heavy Full KYC: $25 reload + ~$10 transactions = ~$35/month. For mixed USD/non-USD: ~$45-$50/month. The schedule makes accurate modeling possible in advance rather than discovery after the fact.

Fee transparency as a signal beyond fees

The reason fee transparency matters beyond the actual numbers is that it correlates with broader operational philosophy. Operators who publish clean fee schedules typically have responsive support, accurate marketing, and reliable operations. Operators who hide fees often hide other things too — limitations, restrictions, operational issues. For users evaluating products, fee transparency is one of the more reliable proxies for overall product quality.

How to evaluate fee disclosure across providers

Practical evaluation steps: read the published fee schedule completely, not just the marketing page. Look for what isn't listed (often the revealing part). Calculate monthly cost on your actual spending pattern using the published numbers. Compare across providers using the same methodology. If a provider doesn't publish a complete schedule or requires you to estimate based on partial information, that's itself a signal worth weighing.

The category convergence on transparency

The crypto card category has converged somewhat on the basic structure (issuance fee + reload fee + transaction fee) but not on transparency. Operators differ on which fees they emphasize, which they obscure, and how much they leave to user discovery. The convergence on structure suggests the basic product is becoming standardized. The non-convergence on transparency suggests operator differentiation will continue to happen on this dimension, with users increasingly able to evaluate operators on transparency as a quality marker.

Discussion

For users evaluating crypto cards or any fintech product: when did you last actually read the complete fee schedule rather than just the marketing? Worth checking whether what you're paying matches what you thought you were paying.

→ Review: https://beexpay.app