Financial Bubbles and Market Crashes: Why Do They Keep Happening?

Financial bubbles are as old as markets themselves and seem to follow an almost predictable cycle of boom and bust-from the Tulip Mania of the 1630s, to the Dot-Com Bubble of the early 2000s, and most recently, the 2008 housing crisis-bubbles inflate until they burst, often leaving in their wake economic hardship and shaken confidence.

But what are the causes of these bubbles? Can they be avoided? More importantly, why do we keep falling into these patterns? This blog goes into some detail on the mechanisms of financial bubbles: why they form, how they burst, and more importantly, what they say about investor psychology.

What is a Financial Bubble?

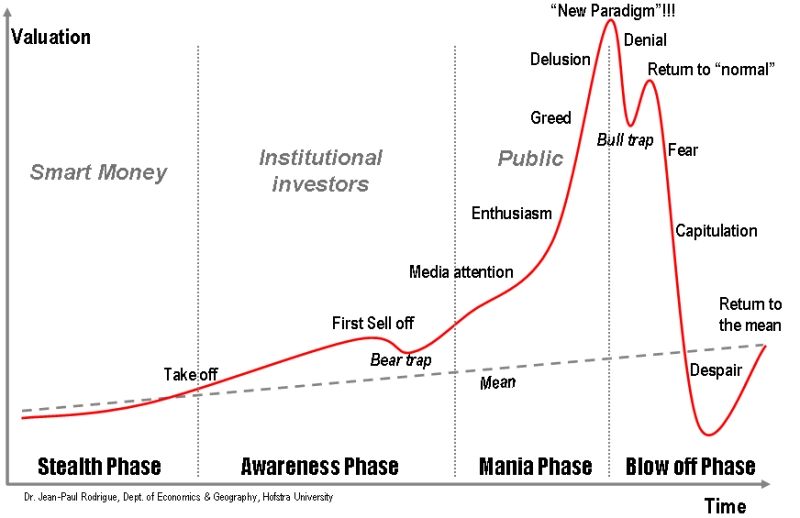

A financial bubble is a condition wherein the price of an asset significantly deviates from its intrinsic value because of speculative purchases. The emergence of bubbles is usually preceded by a steep rise in the price of an asset, probably resulting from some kind of technological innovation, change in policy, or mass enthusiasm. As more and more investors join in, prices keep climbing and further result in what is technically called irrational exuberance-a term very nicely coined by former Fed Chairman Alan Greenspan.

Eventually, the bubble bursts-when a majority recognizes that the asset cannot continue at its inflated value, there is a sell-off that pops the bubble and creates a crash.

Why Do Bubbles Form?

The bubbles are instigated by several factors including:

Speculative Frenzy: Investors pile in, wagering that prices will continue to rise. And so it is with this "fear of missing out" that a self-perpetuating cycle sets in where people buy assets not for fundamental value but because they think someone else will pay more for it later.

Low interest rates and loose credit : When the central banks lower their interest rates, this often spurs increased borrowing and investments. Such cheap credit can flood the market with money and drive asset prices beyond their level of fundamentals.

New Technology or Products: Exotic new technology-the internet in the 1990s or, more recently, blockchain-fosters excitement. When investors perceive others are making fortunes, they often become blind to risk in the hope of comparable gains, moving money into untested assets.

Behavioral Biases and Herd Mentality: It is in human nature, but especially in markets, people tend to herd. Herein, behavioral economists point out that biases such as overconfidence and confirmation bias-when we seek out information supporting existing beliefs-feed the bubbles by creating a sense of certainty that prices keep rising.

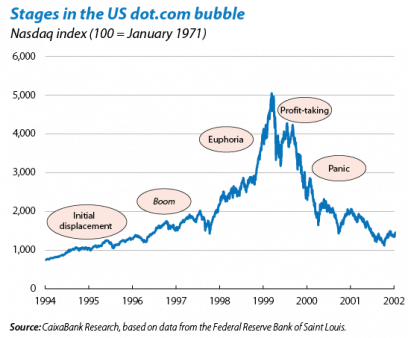

Classic Example: The Dot-Com Bubble

One of the most famous bubbles is the Dot-Com Bubble from the end of the 1990s. The tremendous excitement over the potential of the Internet led to investment in technology start-ups, driving stock prices to unbelievable levels. Many companies had no profits and some had no revenues, yet their stock prices soared. At its peak, the NASDAQ topped 5,000 points at the beginning of 2000, before crashing back down and erasing trillions of dollars in market value.

The Dot-Com Bubble was a lesson in speculative excess. Investors did not consider the long-term viability of many of those internet companies. When reality hit, and people began to understand that most of those startups would not be profitable, it burst.

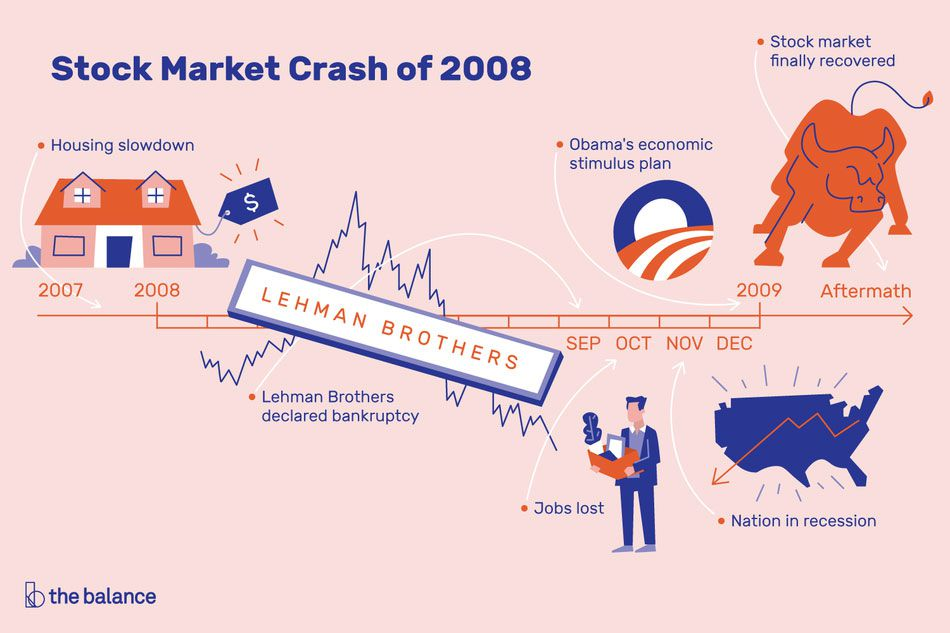

The Housing Bubble of 2008: When Real Estate Went Bust

Another fine example of financial excess was the housing bubble in the early 2000s, though with a more complicated twist. With low interest rates, borrowed money was cheap, and housing prices started to climb. Both investors and homeowners thought that prices would always go up, and banks were more than willing to lend the money. That perpetuated an explosion in home purchases, fueled by subprime mortgages and dicey financial products.

As the housing market cooled, prices began to fall. Homeowners were underwater-owing more than their houses were worth-defaults soared, and the fragility of the financial system was revealed. This was no ordinary bubble-its bursting produced a global financial crisis.

The Aftermath: Why Do Bubbles Hurt So Much?

Because when a bubble bursts, it can have wide repercussions; investors lose money, companies go bankrupt, and in more extreme examples, like the one in 2008, the economy slides into recession. These crashes hurt because they disrupt financial stability, destroy wealth, and often lead to high unemployment and economic hardship.

A bubble does not affect the investors alone. The housing bubble, for example, when it burst, hurt not only the owners and the banks but also whole industries that were linked with real estate, from construction to retail. The after-effects can be sever and long-acting.

Can Bubbles Be Prevented?

Theoretically, bubbles can be tempered by more cautious monetary policies, stricter lending standards, and better financial regulation. But in practice, it's hard to prevent bubbles due to the human factor underlying their causes. When people see others earn huge profits, rationality goes out of the window.

Some economists think that governments should take action once they witness evidence of a budding bubble. However, timing is fraught with problems, and a bit too early intervention may hurt economic growth.

Key Takeaway: The Role of Human Psychology

Bubbles are not about money alone, but also about psychology, more and more economists believe. Behavioral finance is the academic field that combines economics and psychology to explain many of the bubbles that keep happening. Indeed, investors are biased in many ways whereby bubbles become almost unavoidable:

- Anchoring Bias: This is when investors remain anchored to high prices, even when evidence is apparent that they should be falling.

- Availability Heuristic: To people, the sight of other people making money further convinces them that they can pull it off too; irrational investment ensues. FOMO - Fear of Missing Out: The need not to be left behind in profits outweighs sound judgment.

Shall You Worry About the Next Bubble?

The understanding of bubbles and their psychology can also help an individual investor to sidestep really costly mistakes. Since nobody has perfect foresight, being skeptical of "too-good-to-be-true" markets and developing sound investment strategies will help.

Stay Informed but Skeptical: Because the price of an asset is rising doesn't mean that it's worth buying. Research thoroughly and understand the fundamentals before investing.

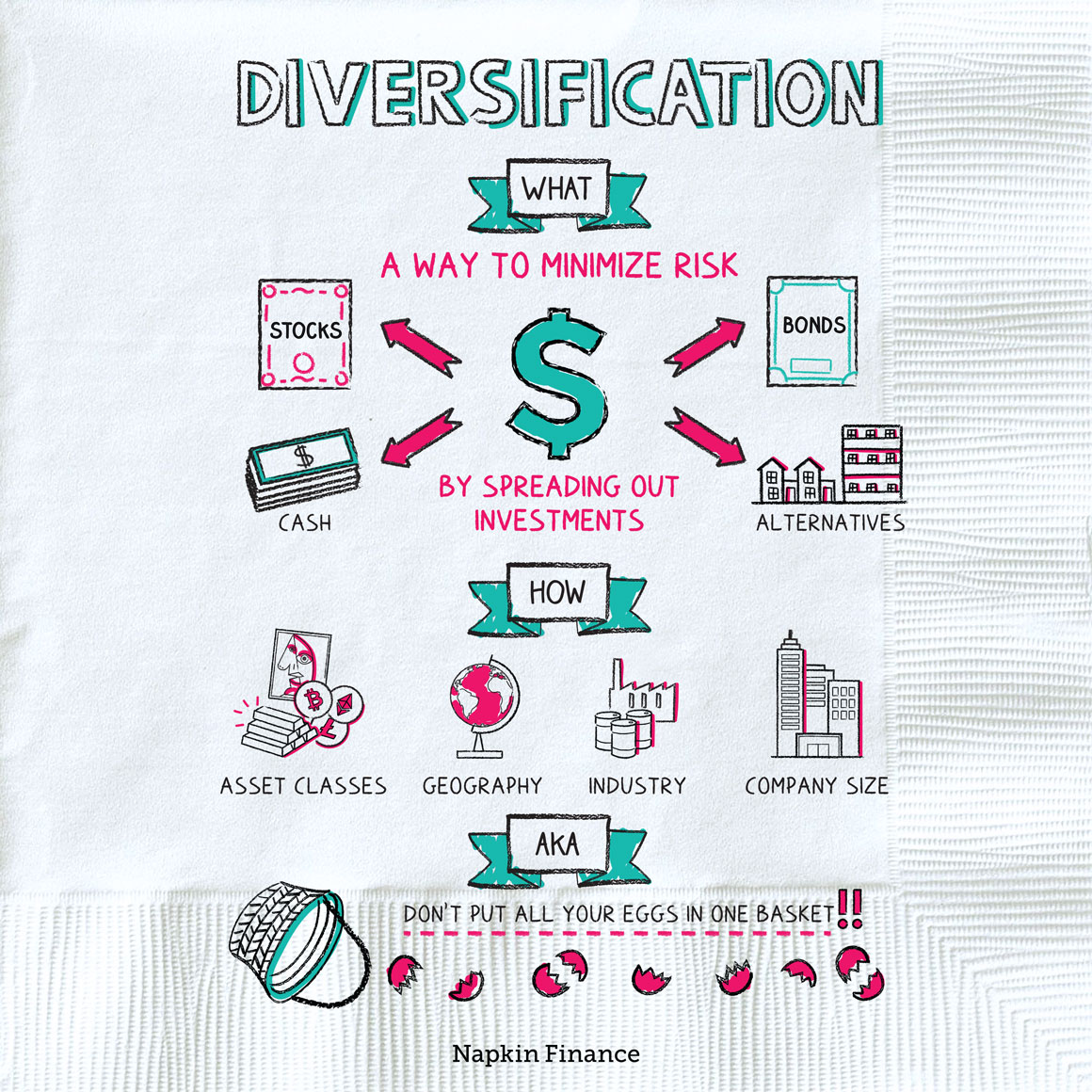

Diversification: A diversified portfolio will take the sting out of a burst bubble.

Have an Exit Strategy: For those high-risk investments, know how you will get out and be ready to execute when things start to go downhill.

Remember the Fundamentals: Invest for the long term in assets with fundamental value, rather than speculate for short-term gains.

Conclusion

While financial bubbles may appear irrational, they are part of the market's natural cycle. Tided by human behaviors, speculation, and sometimes poor regulatory oversight, financial bubbles will continue to be a feature of the financial markets. By understanding why bubbles form and the role psychology plays, investors can better prepare and hopefully avoid getting caught in the next burst.