The Real Math Behind Your Loan EMI (And Why It Matters)

Most people sign up for a loan EMI the way they accept a cookie policy the number looks affordable enough, so they move on. I did the same thing until I actually broke down what that monthly figure is made of.

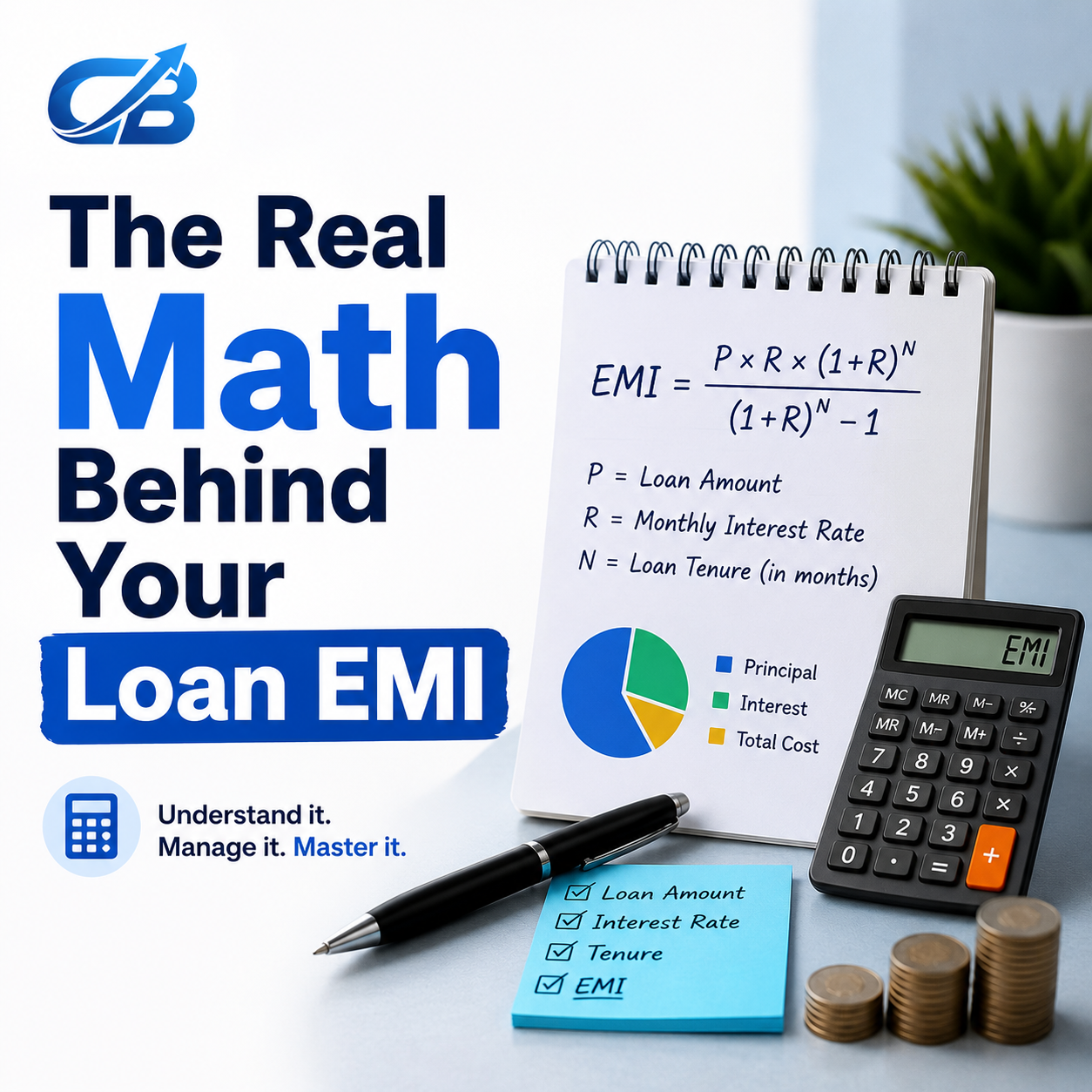

Your EMI isn't one number. It's principal plus interest, recalculated every month as your outstanding balance shrinks which is exactly why the first year of any loan feels like you're barely making a dent. Early on, a much bigger share of your payment is going to interest, not principal.

That's worth understanding right now specifically because the RBI has held the repo rate steady at 5.25% through its last few policy reviews, which has kept new-loan pricing relatively predictable for months a genuinely good window to plan around rather than rush a decision.

Three inputs decide your EMI, and understanding how they interact is genuinely useful, not just trivia:

Principal the amount you're actually borrowing. Obvious, but worth stating: every rupee you don't need to borrow is a rupee you're not paying interest on for years.

Interest rate this is where your credit score does real work behind the scenes. The rate you're quoted isn't a fixed market number; it's the base rate plus a spread the lender sets based on your profile. A stronger score often means a meaningfully lower spread.

Tenure this is the one people get wrong most often. A longer tenure lowers your monthly EMI, which feels like relief, but it almost always raises the total interest you pay over the life of the loan. Stretching a loan from 3 years to 5 years might drop your EMI by a comfortable-looking amount, while quietly adding a substantial chunk to what you pay in total. Lower monthly number, higher total cost both are true at once.

There's a lever most people never touch: prepayment. Even a modest lump sum paid toward principal early in the loan say, from a bonus or a tax refund does more to reduce total interest than the same amount would do later in the tenure, because it's cutting into the balance while the interest-heavy part of the schedule is still running. Check your loan's prepayment terms before you need them, not after.

The most useful thing you can do before signing anything: model it yourself instead of trusting an advertised "starting from" rate, which is usually the best-case number offered to the strongest applicants, not a realistic baseline for you specifically. Run your own numbers through a personal loan EMI calculator with your actual rate and tenure, and compare offers from multiple lenders before you commit rather than anchoring on the first number you're quoted.

An EMI that looks affordable on a lender's landing page and an EMI that's actually affordable for your monthly budget are two different calculations. Only one of them is the one that matters three years from now.

La educación financiera es algo que deberia enseñarse en las escuelas. Post como el tuyo ayudan a llenar ese vacío.