Buy the S&P 500 Index and forget all about it

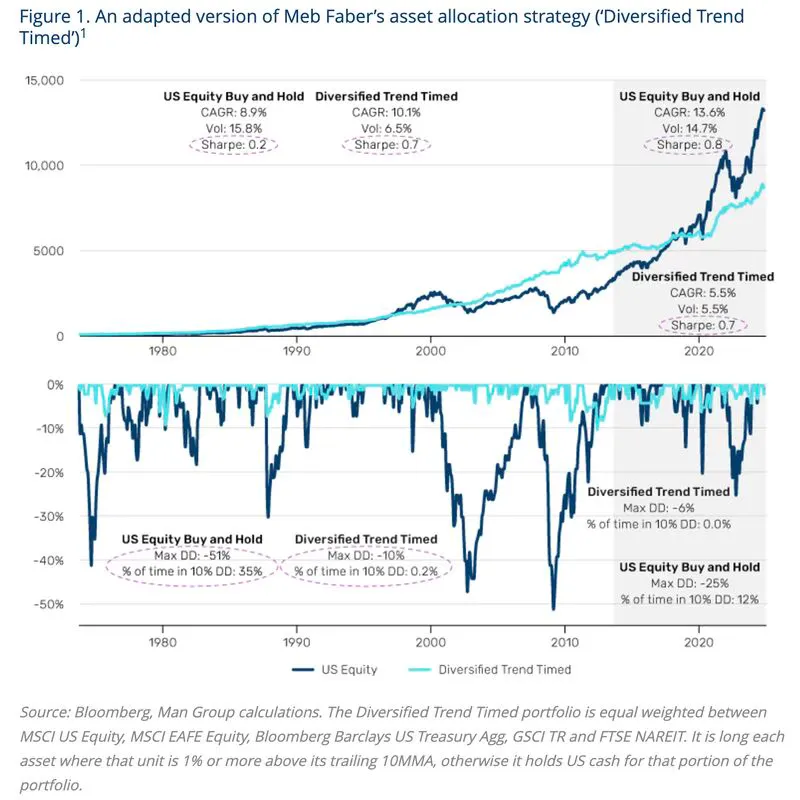

In the paper „A Quantitative Approach to Tactical Asset Allocation“ Meb Faber outlined a simple yet brilliant strategy for asset allocation: equal weight across five liquid asset classes (US stocks, rest of world [RoW] stocks, US Treasuries, commodities and real estate investment trusts [REITS]) for diversification, and time those segments using trend-following. If the asset is trending higher, hold it; otherwise put that segment of the portfolio into cash.

Had you looked back from 2013, you’d have liked what you saw: a Sharpe ratio more than three times that of US equity buy-and-hold (the dark blue line). And most eye-catching, a maximum drawdown a fifth of the magnitude, and spending just 0.2% of the time in a 10% dip, compared with a third of months for US equity buy-and-hold. Since 2013, Diversified Trend Timed has a similar profile, with its risk-adjusted return identical to the old days. But boredom has been the belle of the ball, as the Sharpe of US equity buy-and-hold quadrupled.