The AI Bubble Reached the Point Where Grandparents Are Trading on Margin

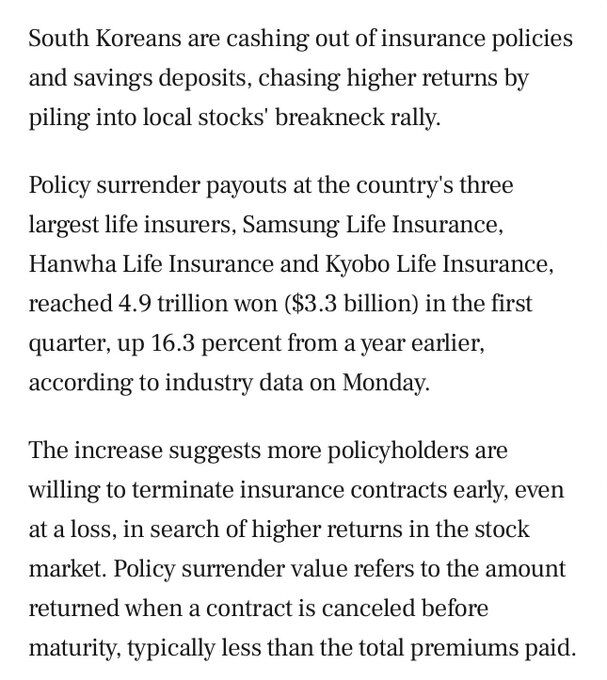

South Korea’s AI rally is entering the phase where societies begin cannibalizing their own financial safety nets to remain inside the boom. Koreans are now cancelling life-insurance policies at a loss to buy semiconductor stocks, savings-bank deposits just fell below 100 trillion won for the first time in four years, commercial bank time deposits dropped another 12 trillion won since February and margin debt on Korean equities climbed toward record highs near $24 billion. Domestic investors have already poured roughly $25.3 billion into South Korean equities this year alone, while leveraged positioning continues accelerating at a pace rarely associated with stable financial environments. The deeper issue goes far beyond speculation itself, because every major bull market eventually attracts speculative behavior, while the truly important signal comes from the source of incoming capital. Early-cycle rallies are usually financed through rising income, expanding liquidity and broad economic optimism, whereas late-cycle rallies increasingly depend on dismantling older layers of financial protection, pushing households toward converting insurance contracts, deposits and retirement buffers into fuel for momentum trades.

The speed of the leverage expansion itself has become extraordinary. Since the start of 2025, margin debt in Korean equities surged roughly 140%, while another 32% increase accumulated just since the beginning of this year, pushing the system toward levels that would have looked unimaginable only a few years ago. To understand the scale of the shift, leveraged bets on Korean stocks stood near only $5 billion back in 2020, meaning the speculative credit machine surrounding equities has multiplied several times within an extremely compressed period. Even those figures likely understate the true size of the exposure because many loans used for stock purchases are increasingly categorized under different forms of borrowing rather than directly recorded as equity leverage. Once a financial boom reaches the point where leverage begins spreading through disguised channels outside the headline statistics, the boundary between visible speculation and hidden systemic exposure starts becoming dangerously blurred.

The atmosphere surrounding the rally now increasingly resembles collective financial escalation rather than normal investing behavior. A Korean civil servant recently posted on Blind, the anonymous workplace app, showing that he had placed 2.3 billion won into SK hynix shares, while 1.7 billion won of that position came directly from margin loans borrowed from his brokerage. He openly described the strategy as an attempt to grow wealth faster through aggressive leverage because he expected the semiconductor cycle to continue into 2028, then returned four days later claiming profits of 267 million won. Around the same time, a Seoul Metro employee in her twenties wrote that rather than missing the rally she was prepared to “risk complete collapse,” explaining that she had used 150 percent margin financing to fully leverage into stocks. Once ordinary salaried workers begin publicly treating maximum leverage as rational career planning, markets are no longer operating mainly through valuation logic because social psychology itself starts becoming the dominant driver.

The demographic shift surrounding this process makes the picture even darker, because investors over 50 now control 62% of margin loans at Korea’s largest brokerages while margin debt among people in their 60s doubled from 3.9 trillion won to 8 trillion won within a single year. These are people who spent decades inside fixed deposits, pensions and real estate, yet many are now entering a semiconductor rally at record highs using borrowed money after years of low yields gradually convinced conservative savers that caution itself carries its own financial punishment. During the March correction, when the KOSPI temporarily fell around 19%, leveraged investors in their 60s reportedly lost roughly 20% on average before the rally resumed upward again, reinforcing the psychological belief that every decline merely represents another buying opportunity. Korea’s AI-semiconductor boom originally looked like a story about industrial power and technological dominance, but the surrounding financial behavior increasingly resembles a society attempting to defend purchasing power through participation in asset inflation. The entire environment quietly began signaling that cash leads toward stagnation while leveraged exposure appears to offer the only remaining path toward preserving wealth, status and future security.

And every part of the system is now incentivized to keep the machine running. Korea’s ten largest brokerages generated roughly 600 billion won in interest income from margin lending during the first quarter alone, representing a surge of almost 56% from a year earlier, while investors continue borrowing at annual rates between 7% and 9% simply to increase exposure to semiconductor momentum. At the same time, major financial institutions continue reinforcing the optimism surrounding the rally, with J.P. Morgan recently raising its base-case KOSPI target to 9,000 and projecting a possible move toward 10,000 under a bullish scenario tied to a prolonged AI-memory-chip cycle. The combination becomes psychologically powerful because rising prices validate leverage, leverage accelerates prices further and institutional forecasts gradually transform speculation into something that begins feeling socially sanctioned and economically inevitable.

This is how late-cycle psychology mutates once participation in the rally stops feeling optional and gradually turns into a form of social pressure. Markets slowly lose their role as mechanisms for allocating productive capital and increasingly behave like systems rewarding whoever accepts the highest exposure to risk, forcing households to buy assets less because valuations remain attractive and more because everybody around them appears to be compounding wealth faster than wages, pensions and deposits can realistically follow. Once insurance policies themselves become liquidity sources for semiconductor momentum trades, the distance between investment mania and systemic fragility narrows extremely fast because societies begin consuming tomorrow’s stability in order to maintain today’s participation in the boom. Something similar is already emerging in India through MTF leverage and retail speculation, only in a smaller and earlier form for now, yet the emotional pattern remains almost identical as households gradually exchange future stability for present exposure because asset inflation became socially impossible to ignore.

P.S. Interesting read:

https://www.koreatimes.co.kr/amp/economy/20260517/brokerages-hit-jackpot-as-retail-investors-borrow-more-to-chase-koreas-stock-rally

What is happening in South Korea increasingly resembles a more extreme version of something already visible in India: foreign capital exits while domestic money keeps the market levitating.