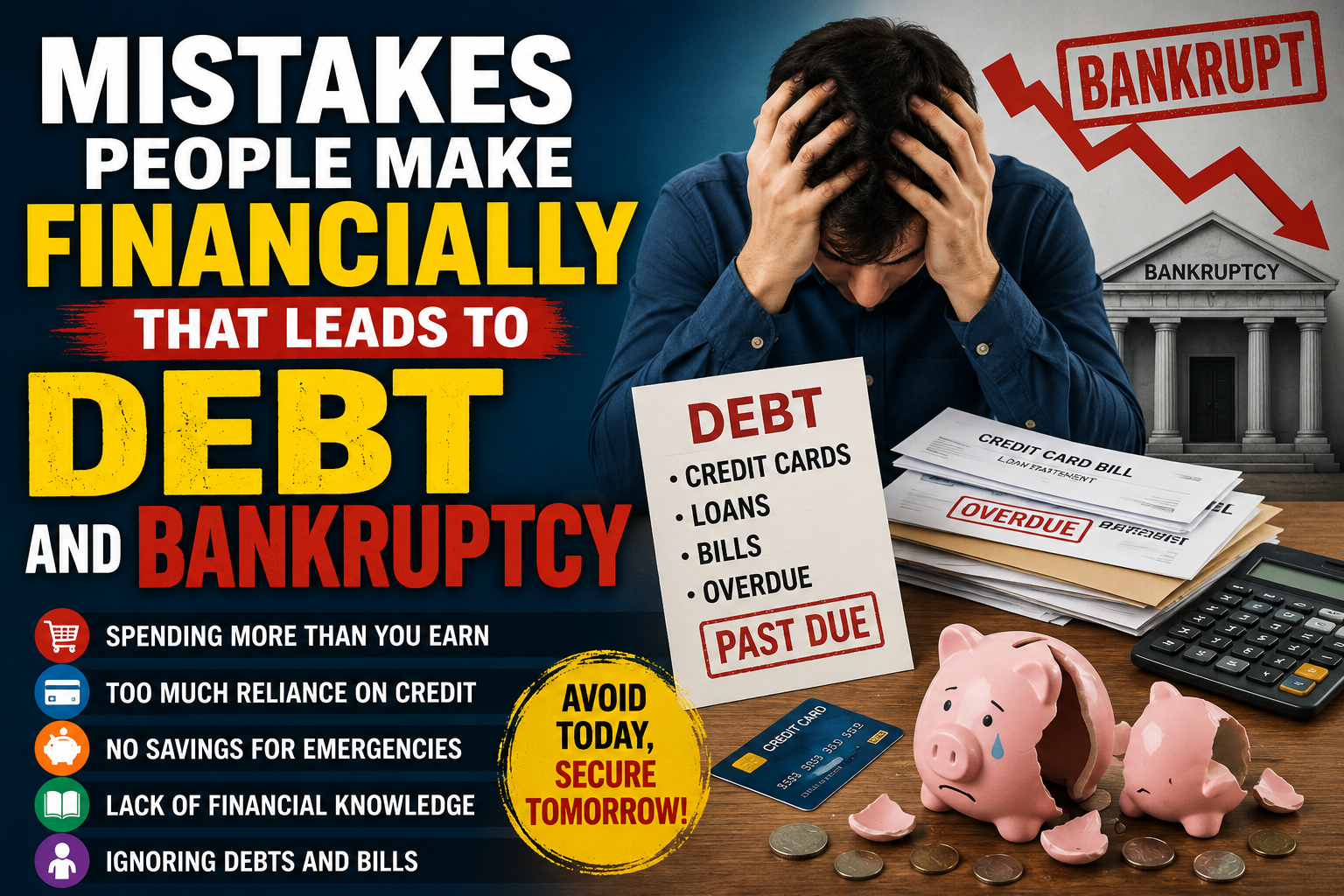

Mistakes People Make Financially That Lead to Debt and Bankruptcy

The use of money is a vital part of our lives. It is necessary to finance food, rent, education, health care, transportation, etc. With good money management, life is less stressful. But lots of individuals commit monetary blunders that gradually trap them into being indebted. These errors can happen again and again and will eventually cause bankruptcy if they are not addressed for an extended period. Bankruptcy occurs when an individual or business is unable to pay their debt. I think most financial issues don't occur in a flash. They tend to make minor errors which are overlooked until they reach critical status.

The No. 1 "rule" is that people spend more than they make. There are people who wish to have a lifestyle which they are not ready to afford. They spend lavishly on clothes, phones, cars, and other luxury things that they may not afford. Rather than being able to afford them, they take out loans to cover their expenses. This leads to un-necessary debts. I have come to find out that it is better to go through life simple than to try to impress others with things I can't afford.

The next common error is not having a budget. Budgets allow individuals to understand where their money is going and the amount of money that is coming in. When one is without a budget, people tend to spend unwisely without knowing it. The little things that we spend from day to day may not seem like much but they can really add up. Before they realize it, they have run out of cash for the essentials. While having a budget helps to make it easier to pay your bills and save for the future, it also helps to "control your spending.

In many cases, people also do not save any money for emergency purposes. Life is unpredictable. One can suddenly be out of work, ill or have a surprise repair invoice. The only alternative is to borrow money if there is no emergency savings. This can easily turn into a burden, particularly if additional emergencies arise prior to the debt being repaid. As a rule, I tell myself that it's better to save a little bit each month than nothing at all.

One error is over-dependence on loans and credit. There are times when you will need to take out a loan, and there are times when you will not need to take out a loan, but borrowing for unessential items isn’t a wise plan. Some people acquire loans merely to purchase products that they want rather than that they require. They also spend money on credit recklessly, without considering the interest rates that they will have to be paying off. The more interest that accrues, the more the debt will grow and the more difficult it will be to pay it back. This can cause entrapment in the cycle of borrowing and paying back that is difficult to break free from.

Lack of financial awareness is also a significant reason for debt. A lot of people don't take time to learn how to save, invest, or budget or pay debt. As a result, they tend to make bad financial decisions. Others fall victim to scams or false investment tips promising easy and fast money. Others put the money they have saved into ventures that they haven't thoroughly researched. My belief is that one of the best investments one can make is in personal finance education – knowledge can prevent expensive errors.

Also, there are those who avoid paying their debts as early as possible. They ignore bills, don't answer lenders' calls, or do not accept any responsibility for the situation. Unfortunately, there are interest and penalties that allow unpaid debts to grow over time. A little debt can grow into a lot of debt in a couple of months or years. Early intervention when money matters are a concern increases the potential to find a solution before things get really bad.

A second financial error is running around trying to be as rich as everyone else. With the advent of social media, this is an even more prevalent issue. They see people traveling around, buying luxurious items, and they feel like they have to do so as well. There are those who borrow money simply for show. What is real is that many people only put their best photos and videos on social media and conceal their financial problems. I've learned that I shouldn't compare myself to anyone because it will cause more stress. It's better to think about my own financial objectives.

Lack of patience is also a serious financial mistake. There is a great deal of desire among individuals to make loads of money in a solitary blink of an eye. Due to this, they look for unrealistic investments and bogus schemes that offer quick and big profits. Many tragically end up with little or no savings and with debt. It takes time, discipline and effort to build wealth. There really aren't any shortcuts to financial success.

Not planning for the future can also result in financial stress. When you don't think about retirement, education, or other obligations, some spend their entire income. As the years go by, they are burdened due to lack of savings and investment. Financial planning can support individuals to plan for future needs and minimise the risk of being in debt later in life.

To wrap things up, debt and bankruptcy are likely to occur due to a series of financial errors, as opposed to a solitary one. Over spending, not budgeting, not saving, borrowing too much, not knowing about money matters, not paying off debt, gambling with other people, and the pursuit of quick money, are all financial blunders that can lead to financial instability. Fortunately, these blunders can be avoided by following some simple financial guidelines, being disciplined, and patient. I think everyone can make smart financial decisions today that will benefit their finances in the long run. There is nothing easy about tracking your cash but it is among the finest ways to find tranquility, financial freedom and a safer future.