SLC32-W2 || Real Life Problem Solving Challenge: Budget Planning

We live in the era where most people earn from diverse sources of income or have diverse sources of income. I'm one of those people whose income isn't stable and fixed. Why? Because I do a lot of things that gives me money and these things don't pay me fixed income.

There may be days I earn $70 monthly in one month from one of my skills and other skills give me a different income. All I know is that I don't earn a salary, but that doesn't mean I don't have an estimated income annually and doesn't also mean I can't make a budget for my income, coming in and out. This is how I plan my income as a multi-stream income earner.

How do you plan your weekly or monthly budget? Explain well. |

|---|

Everything now is digital and this makes even more sense that I can plan my monthly and weekly budget without having to sit with a pen and paper to do that. I'm still under the roof of someone, not paying rents and feeding, but I do have a budget because even though I'm still under someone's roof, I spend a whole lot, sometimes, out of my budget, but what I'm going to share with you has helped me to be disciplined and will also help you. I do plan my monthly or weekly budget in different ways.

How? |

|---|

Knowing my sources of incomes and what they can produce monthly: I'm into photography, video editing, graphics design, crypto trading, content writing on steemit, tailoring, academic mentorship, side hustles that are stable and lot more and all these pay me because it's my skill and I implement it anytime I want to. So I can't tell my total income. I can only estimate my total income which ranges from 250k - 600k monthly.

Estimated income*: Having an estimated income can actually help me to know how much I'm spending, how much I'm saving and how much I'm investing because I invest a lot.

| Knowing my sources of income |

|---|---|

| Taking note of my expenses |

Taking note of my important expenses

If I don't get know what expenses are important to me, I'll end up spending out of my budget for the month even though the money comes daily and weekly. It's better to budget higher and have surplus than to budget lower and have deficits. These includes;

| Category | Amount in naira |

|---|---|

| Data purchase | 50k |

| Content creation | 30k |

| Transportation | 10k |

| Body amenities | 20k |

| Fuel for laundry | 10k |

| Contributions | 10k |

| Shaving | 5k |

| Emergency funds | 30k |

| Savings | 50k |

| Investment | 35k |

| Total | 250k |

Now, I always ensure that my data, fuel for laundry, content creation, emergency and transportation money are budgeted from the surplus of last month since I don't earn salary but have estimates of my money. My non-essential expenses are from my income in that month, probably towards the last week of the month after keeping my main income.

For example in May, I had over 500k as income from my various sources and what was left over after spending was 300k. I didn't spend much last year and my investment yielded profits for me. So that's the surplus I'll be using to budget this month until the money for this money start coming in as it's already doing. I do budget two days before the next month.

In most cases, I use the 70/30 rule which is for expenses(needs, emergencies and wants) and 30% goes to savings for raining days.

Tracking my income and expenses helps me know what I've spent especially when I'm using different back apps. I usually do it weekly to see the money coming in a particular week and the money leaving my account and I'll then balance it from what was budgeted for the month in terms of certain expenses so I don't go beyond my budget. Those extra weekly income that comes in are used for settling wants since it's not part of the budget.

What tool or method do you use to track your expenses? Show at least one tool or method in detail with a selfie. |

|---|

Have you heard of Kuda banking app? Banking apps today is really helping us track our expenses and I'll say this particular app is the best because it does spend and save and you can budget your money in flexible points instead of mixing the money for transportation with that of food or data.

| Method 1 |

|---|

It's just like the digital envelope method that's the best and investments can be done here. I'll share two methods and then explain one practically and in details. I've not been used to tracking my expenses by writing them down on a piece of paper even though it's effective. I'd rather use a notepad and the digital banking app that automatically plans for me and keep me on track.

- Kuda banking app

- Recording and calculating using my Notepad from my bank app

To track my expenses using the kuda bank app, I use the spend and save options. The spend and save options helps for savings when I'm spending out of a budget because I get to save 20% from what I spend. I've been using this pattern before using their savings option.

This savings option is one of the best things that has happened to me. I can apportion my expenses in these flexible savings and spend it individually without making collective spending. What do I mean?

| Saving Option |

|---|

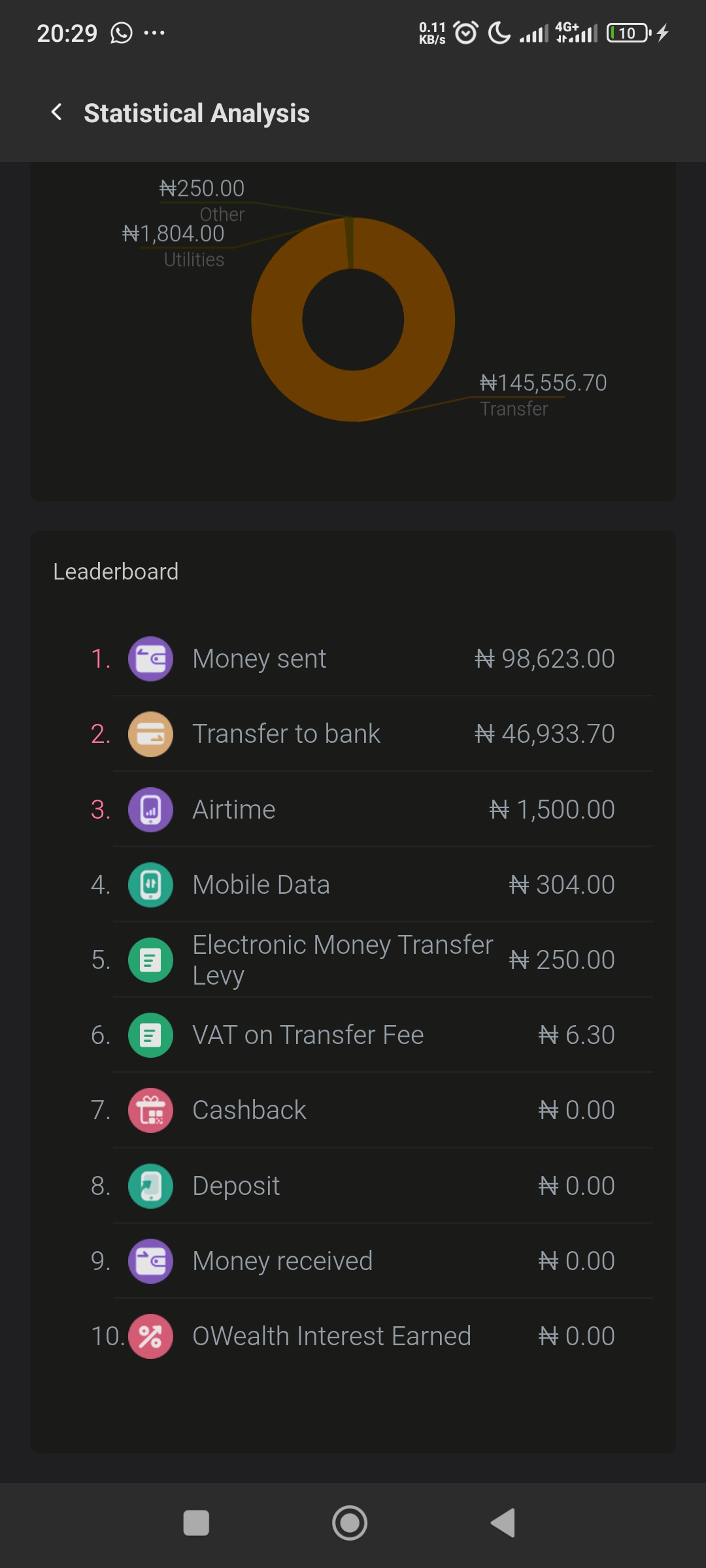

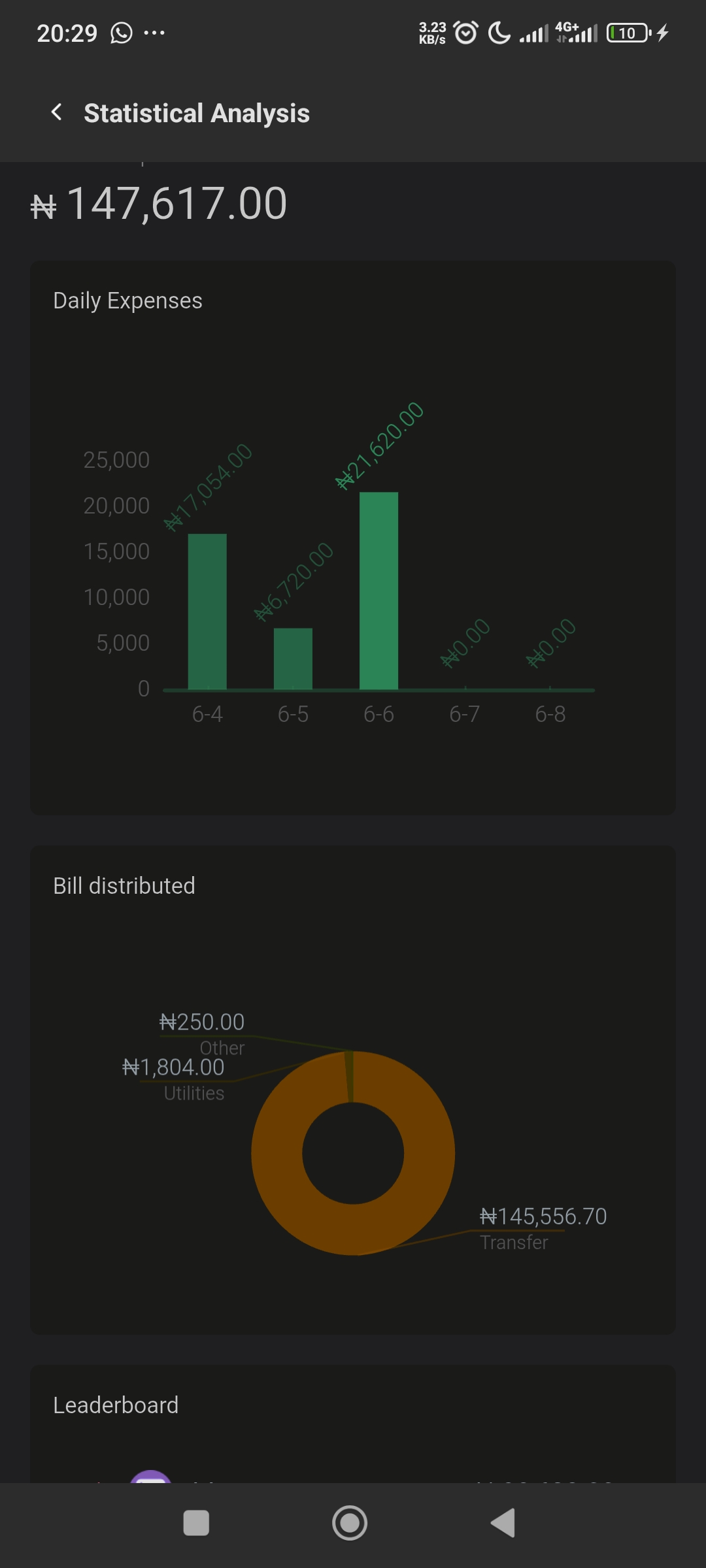

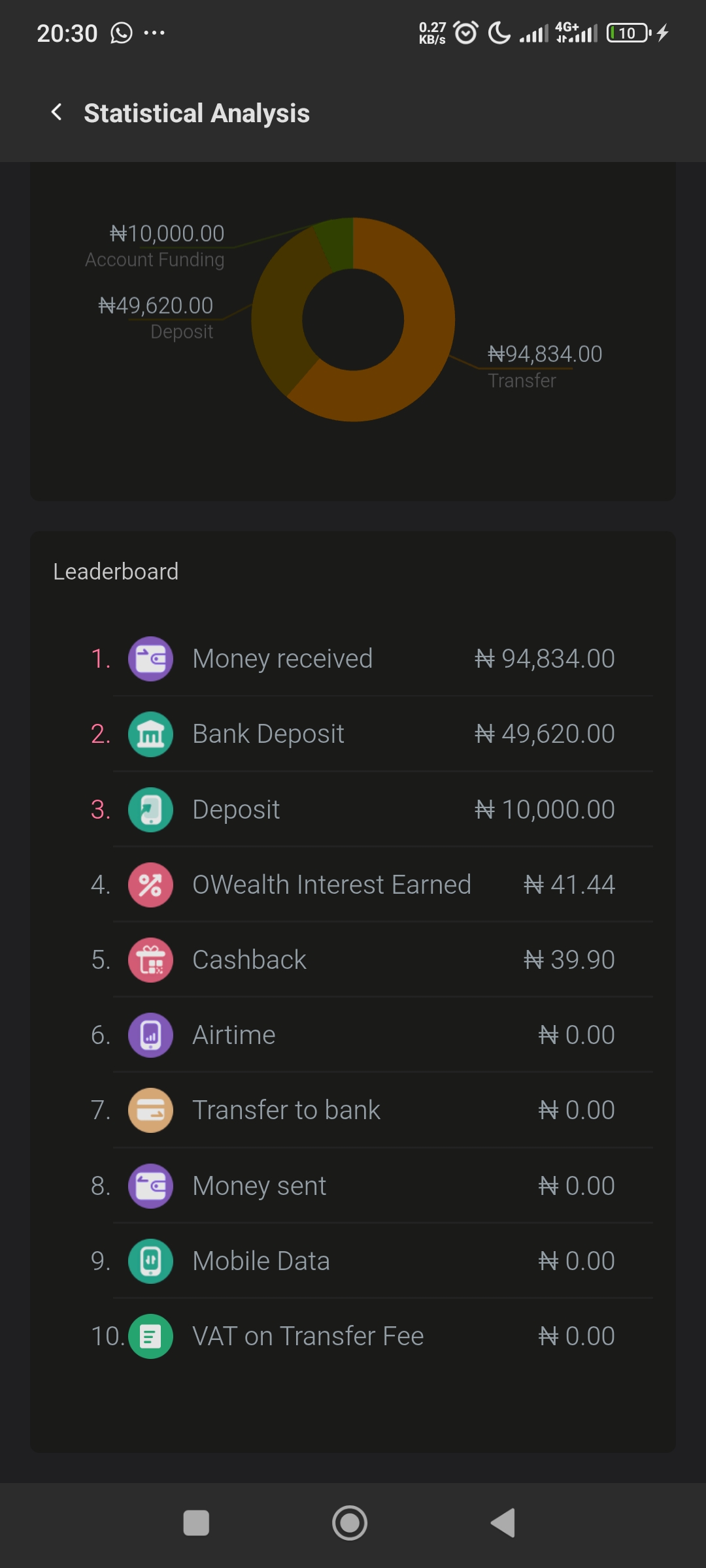

Let's check this out. In my flexible savings, I'll send money for data and label it so that if I want to spend, I'll just remove it from there. As for transportation, I'll send 20k there. Anytime I want to expend on transportation, I'll just go to the transportation savings and remove what I want to use. The savings option has transaction records of what is removed and when it was removed. So if I want to go into details, I'll just refer to where I removed the money from and when.

Check this out. You'll see a list of all my expenses and the amount isn't shown because of security reasons. I'm just using this to be illustrative in telling you how I track my expenses.

| Lists of all my labelled Expenses |

|---|---|

| I can add money and also withdraw from individual expenses |

I don't need to worry about spending too much because I remove my money from where I budget. This is the best and it eliminates the use of note pad or writing out your expenses using your bank statement. It saves time and is stress-free.

| Selfie with method 1 |

|---|

The app has statement in the savings option based on what you label. If you have 5 expenses, you'll send money and label it so you'll know the money to remove anytime you want to remove it. It also has records of when you removed it. For example.

| Data purchase | 20k |

|---|

If I want to buy data, I won't remove it from my total balance. I'll just go to the savings option, remove it from there and send to main balance. This helps in disciplining my spending habits

Method 2 |

|---|

For the note pad method, this too is essential for making calculations to know how much is spent. I usually use this when spending on my wants because I have two accounts where my money enters. So when the money enters in my second account after budgeting with the first, I spend on wants, side hustles and trading.

|  |

|---|---|

|  |

So I'll use my notepad to list them starting from the beginning of the month and I do so weekly so I'll know how much is leaving the account and how much is entering. This is a picture and a rough sketch.

Opening balance: 181k

I use the bank statement and the statistics to get my expenses in check and see what and when I expended them. Like I said, this is for my wants, sending to people who wants to sell crypto, side hustle, trading and sometimes airtime and other utilities.

| Date | Description | Amount |

|---|---|---|

| June 1 | Black Senator wear and shoes | 67k |

| June 2 | Dollars for bybit | 55k |

| June 3 | Rough investment | 30k |

| June 4 | Buying stem from a friend | 29k |

| June 4 | Transfer to a friend | 940 |

| June 5 | Data and charges | 560 |

| June 5 | Airtime recharge | 1500 |

| June 6 | Nill |

These are my expenses. My total income remains 353k as I had 181k as opening balance and 172k income. So if I'm to subtract from my expenses, what will remain is 170k as balance.

|  |

|---|

What are the unnecessary expenses that affect your income? Explain. |

|---|

I do have unnecessary expenses that affect my income and these expenses are seen in my second account.

- Buying Junks: Most times when I'm bored or want to eat, I'll just want to spend it on junks like chicken, snacks or drinks and others. These aren't important, but just some cravings I usually satisfy.

- Social media contents: I have this routine of preparing a different recipe every Tuesday just to grow my page. This would require me to spend money that I didn't plan to spend on food ingredients and the likes.

Giveaways and loans: Sometimes friends ask me to help them out with money to take care of urgent need. I didn't budget for this, it just came up and I had to face it squarely.

Unnecessary spending of data: The money is usually budget for data doesn't last me for a month because of movies I download, editing on Capcut and other data consuming apps. So I'll spend the money without unexpectedly

The thing is that I don't usually spend much because I'm always indoors and rarely go out.

How do you save money from your income that will sustain you for future hardships? |

|---|

I usually use Kuda Bank to do fixed deposits so I'll not have to touch them. Every month, I keep topping up and gaining interests from it. If I save 90k, I'll get 10k as my profit in a month which is very much profitable without risks.. So from January to June, I've been saving 30k. 30k gives me interests of 4k every month.

| Savings amount | Interest in a month |

|---|---|

| 30k | 4k |

| Saving in 6 months | Interest in 6 months |

|---|---|

| 180k | 24k |

That's not bad because of how much I'm saving. If I get to save more on a monthly basis, that's good money.

Aside from saving it here, I invest my money in crypto and stocks. Kuda Bank app helps me see stocks I can invest in on a short-term and long-term without losses while in crypto, I purchase coins and keep them as long as I want. If the profit is good enough, I convert to stable coin for future purpose.

| Investing in stocks and crypto |

|---|---|

| saving |

So like I said, I usually remove 30k from my income and budget it on savings while the money in my spare account is used for trading, investments in crypto and stocks for the long-run. Investments like this makes me stick to my budget and don't allow me spend unnecessarily, knowing well that rainy days are coming.

Have you ever created a budget that would improve your financial situation? Show us practically how. |

|---|

Yes I've done that and it's to curtail my expenses in certain things. You know when you have the money in excess, you'll want to spend until you spend and realise you've overspent. So sticking to a good budget had helped me stay disciplined on certain things. Let me illustrate using this table. Let's talk about my expenses for last month.

I've been spending more on data, content, and transportation. So I decided to cut them down on budget. Last month, these were my budget.

May

| Data purchase | 60k |

|---|---|

| Content creation | 40k |

| Transportation | 35k |

| Savings/investment | 30k |

| Total | 165k |

June, 2026

| Data purchase | 50k |

|---|---|

| Content creation | 15k |

| Transportation | 10k |

| Savings/investment | 90k |

| Total | 165k |

If you notice, my savings and investments is 90k from reducing the cost of those expenses listed there. I've been able to manage my money instead of spending it because there's excess and it comes everyday. I've also been able to save with a huge amount.

What advice would you give to others for great budget planning? |

|---|

We have different types of income earners and that's where my advice would come from. For salary earners, to have a good budget planning, you need to follow the following.

You'll need to set a budget that can accommodate your salary and always prioritise savings even though it's barely enough. 5k can go miles.

Track your expenses after the month and don't spend much on paying debts as this won't help you create a feasible budget.

- Spending unnecessarily from someone's money and then agreeing to pay back from your salary will put you in a tight situation and won't help you budget for anything because by the time your salary drops, it's already going for debts. So avoid getting loans for unnecessary things. You can always live with your means except in cases of emergencies. I know people who get loans to spend on things that aren't worth it, afterall salary is coming.

For those not earning salaries

- Track your expenses even though your income comes daily or weekly to avoid overspending because there's money

- Allocate your funds, label it and invest for rainy days because it's not every month that may be favourable to you. So savings will help you those periods.

_Differentiating between wants and needs will help you know how much to spend on these two to avoid regrets later. People spend money and then regret later that they wouldn't.

People have different tastes of spending, but the 70%/30% rule can still apply. You can save up to purchase things in the future with 30% of your income that comes and be disciplined.

- Plan your life. Write down things you want to achieve in a month with your money. You can budget for a lend and then use the saving option to keep it there to avoid usage. This will help you do a lot of things as most people end up earning high, but can't see anything useful they use the money to do other than spending on groceries and all that.... I hope my advice finds you well.

Comments on other people's posts |

|---|

https://steemit.com/hive-170554/@bossj23/tg9ten

https://steemit.com/hive-180106/@bossj23/tg9tk4

All screenshots are from my phone's apps

I invite @pasindukd @shahidalinaz and @photoworker

Saludos apreciado amigo. Creo que muchas personas actualmente tienen salarios variados o diversas fuentes de ingreso. Así también vivo yo y se que así es un poco más difícil de coordinar un presupuesto pero siempre es necesario hacerlo y así poder tener una buena administración y finanzas. Te deseo éxitos

0.00 SBD,

4.94 STEEM,

4.94 SP

Thank you Sir. Sometimes we don't even remember to do the budgeting because such time isn't there. I see why most people need a financial manger. 😁😁

https://x.com/i/status/2063667819099656676

you haven't still replied my comment on my post..... you asked me about having any guidelines