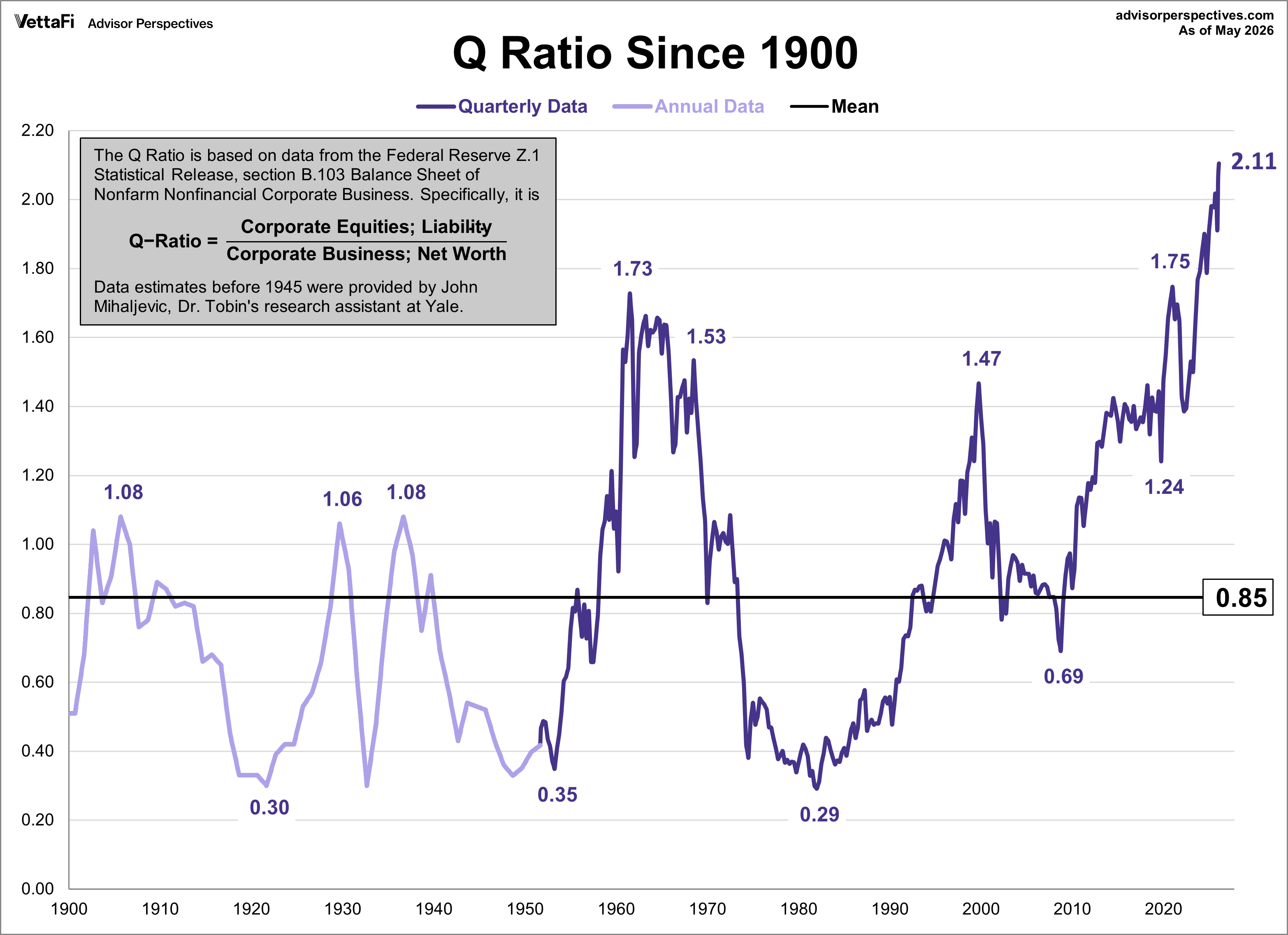

Can You Time the Market? James Tobin Had a Better Question

In 1969, Nobel Prize-winning economist James Tobin introduced a deceptively simple idea that challenged one of Wall Street's most deeply entrenched beliefs, namely the assumption that predicting future price movements should occupy the center of every investor's decision-making process. Rather than asking whether stocks would rise or fall over the next month, quarter or year, Tobin focused on a far more fundamental question: what are investors actually paying for when they purchase shares? The answer became known as the Q-Ratio, a valuation metric that compares the market value of companies with the replacement cost of their underlying assets, thereby providing a framework for evaluating whether stocks are being purchased at reasonable prices. In practical terms, if investors are paying two dollars for every dollar of corporate assets, the market may be expensive, whereas if stocks trade below the replacement value of those assets, opportunities may be considerably more attractive.

The concept stands in direct opposition to one of the most popular investment strategies ever created: market timing. Every generation produces investors who become convinced that they can successfully avoid major downturns, sidestep crashes and re-enter the market immediately before the next bull run begins, largely because the logic appears irresistible when viewed from a distance. After all, why would anyone willingly endure a 30%, 40% or even 50% decline if a timely sale could preserve capital and allow for repurchasing shares at much lower prices? The challenge, however, is that markets rarely provide advance notice before making their largest moves, which means that a strategy appearing flawless in theory often becomes extraordinarily difficult in practice.

While identifying market tops and bottoms is remarkably easy with the benefit of hindsight, investors operating in real time must make decisions while uncertainty remains high and information remains incomplete. Even more importantly, some of the most powerful gains in stock market history have occurred during relatively brief periods that very few investors anticipated beforehand, which creates a dangerous problem for those attempting to move in and out of the market. If the strongest advances tend to arrive when fear remains elevated and sentiment remains fragile, how many investors are realistically positioned to participate in those gains? The answer is often fewer than expected, which helps explain why market timing frequently disappoints despite its intuitive appeal.

The arithmetic supporting this conclusion is difficult to ignore. A long-term investor who remained fully invested throughout the market's advances, corrections, recessions, recoveries and occasional panics would have transformed a modest sum into extraordinary wealth over the course of the twentieth century. Yet those impressive results were not generated evenly across thousands of trading days, because a surprisingly small number of exceptional months accounted for a disproportionate share of overall returns. Missing only those critical periods would have reduced lifetime investment performance by an astonishing amount, thereby turning extraordinary wealth creation into something far more ordinary. The challenge, therefore, extends beyond avoiding losses, because investors must also avoid missing the gains that ultimately drive long-term compounding.

This is where the discussion becomes considerably more sophisticated than the traditional debate between market timers and buy-and-hold advocates. Andrew Smithers and Stephen Wright, the authors of "Valuing Wall Street", argued that investors often focus on the wrong question when discussing market timing, because the real issue is not whether prices will move higher or lower tomorrow. Instead, they suggested that investors should focus on valuation and should continuously evaluate whether stocks are trading at levels that can be justified by underlying fundamentals. Their preferred tool for conducting that analysis was Tobin's Q-Ratio, which they viewed as one of the most effective methods for measuring broad market valuation.

The distinction between momentum investing and valuation investing is far more significant than many investors realize. Momentum investors purchase assets because prices are rising and because they expect those trends to continue, while valuation investors focus on the relationship between price and underlying worth. One approach assumes that recent price behavior contains useful information about future price behavior, whereas the other assumes that extreme deviations from fair value eventually correct themselves over time. Although both approaches have experienced periods of success, they are based on fundamentally different views of how markets function and how investment returns are generated.

History provides compelling evidence regarding the importance of valuation. Before the collapse of the technology bubble, the Q-Ratio reached levels indicating that stocks were trading at extraordinary premiums relative to the replacement value of corporate assets, even as optimism continued to dominate investor psychology. Market participants remained enthusiastic, speculative behavior intensified and prices continued climbing despite increasingly stretched valuations. Eventually, however, the relationship between price and value reasserted itself, leading to one of the most significant market corrections in modern history. The lesson was not that valuations can predict precise turning points, but that valuation extremes eventually matter.

Today, the signal generated by the Q-Ratio is even more striking. As of May 2026, the ratio stands at approximately 2.11, representing the highest reading ever recorded and placing current valuations well above levels observed during previous market cycles. In practical terms, investors are paying more than twice the replacement cost of corporate America, while the market trades roughly 149% above its long-term historical average and approximately 178% above its historical geometric average. Such numbers do not guarantee poor returns tomorrow, next month or even next year, but they do suggest that future returns may be constrained by the exceptionally high prices investors are currently willing to pay. When valuations reach levels never before observed in financial history, should investors continue assuming that future returns will mirror the extraordinary gains of the recent past?

One of the most important lessons investors can learn from valuation metrics is that they are exceptionally poor short-term timing tools. Markets can remain overvalued for years and some of the strongest bull markets in history have occurred after valuations had already reached levels that many observers considered excessive. Valuation provides insight into long-term return expectations, but it offers very little guidance regarding what will happen over the next several months. Investors who expect valuation metrics to identify the exact timing of a correction are often disappointed because markets operate on timelines that frequently ignore logic, patience and historical precedent.

This distinction matters because many investors misuse valuation data in ways that lead to costly mistakes. Upon seeing an expensive market, they immediately conclude that a crash must be imminent, despite abundant historical evidence demonstrating that overvaluation can persist far longer than anticipated. Liquidity, optimism, technological innovation, productivity gains and favorable economic conditions can continue supporting elevated prices for extended periods, even when valuations appear detached from underlying fundamentals. As a result, expensive markets can become more expensive, just as cheap markets can remain cheap for much longer than expected.

At the same time, dismissing valuation entirely carries its own risks. The message of the Q-Ratio is not that investors should liquidate their portfolios and wait indefinitely for a market collapse, because such an approach creates its own set of challenges and uncertainties. The more important message is that starting valuations matter, particularly when evaluating future return expectations over periods measured in years rather than months. When investors purchase assets at historically extreme valuations, they effectively reduce the margin for error and increase the likelihood that future returns will fall short of historical norms. The higher the starting valuation, the more difficult it becomes for future performance to match the impressive returns generated during previous decades.

This reality creates an uncomfortable dilemma for investors today. The greatest risk may not be an immediate market crash, nor may it be a sudden economic shock capable of triggering widespread panic. A more subtle risk exists in the possibility that investors continue extrapolating the recent past far into the future despite valuations residing near unprecedented levels. If future returns ultimately depend on the price paid today, how much future performance has already been pulled forward by investors willing to pay record prices for corporate assets?

More than half a century after James Tobin introduced the Q-Ratio, the question he posed remains as relevant as ever. While investors continue debating interest rates, economic forecasts, technological revolutions and market sentiment, the underlying issue has changed very little. Every investment ultimately comes down to the relationship between price and value, because even the greatest asset can become a poor investment when purchased at an excessive price. Tobin's enduring contribution was not providing a method for predicting the next correction, but providing a framework for asking a question that every investor should consider: how much are we paying relative to what we are actually receiving?