The great leverage experiment: Korea was never the exception

The argument that South Korea's stock market boom may ultimately produce a poorer and more dependent workforce can easily be dismissed as a uniquely Korean story, shaped by the country's demographic collapse, aging population and increasingly desperate search for economic growth.

Such a conclusion would be comforting because it would confine the problem to a single country and a specific set of circumstances. Yet a closer look reveals something far more troubling - Korea is not the exception. Korea is merely one of the most visible examples of a much broader phenomenon that is unfolding across developed economies, particularly in the US, where regulators, financial institutions and policymakers have spent years encouraging households to assume ever greater levels of financial risk while presenting this process as democratization, innovation and financial empowerment.

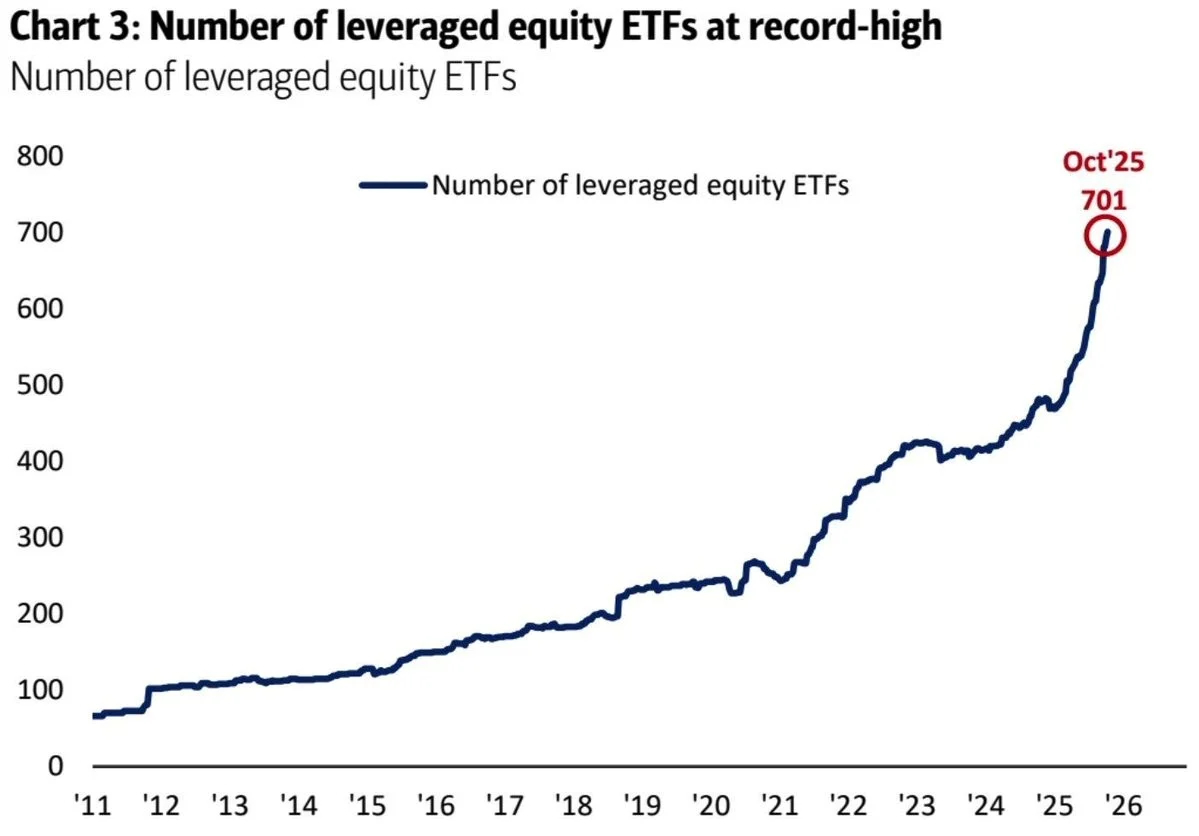

The defining characteristic of modern financial markets is no longer speculation alone but leveraged speculation. Traditional investing once involved allocating savings into productive assets and allowing time and compounding to generate returns. Today's environment increasingly revolves around amplifying risk through leverage layered upon leverage, creating a system in which ordinary investors are no longer merely buying assets but are purchasing magnified exposure to increasingly concentrated bets. Margin debt has reached historic levels relative to disposable income, speculative options trading has become mainstream and leveraged ETFs now allow investors to multiply both gains and losses by factors that would once have been considered suitable only for professional traders. Even more remarkably, many of these leveraged products are themselves purchased on margin, creating a financial structure that resembles a pyramid of leverage rather than a foundation of savings.

The US demonstrates this evolution particularly clearly. Investors are no longer satisfied with buying stocks, instead they buy options on stocks, leveraged ETFs tracking stocks, leveraged ETFs tracking cryptocurrencies and in some cases leveraged ETFs that are themselves purchased using borrowed money. The financial industry continues pushing the boundaries further, with proposals for products capable of generating 5x the daily movement of already volatile assets such as Nvidia, Tesla, Palantir, Bitcoin, Solana and XRP. What makes this trend especially significant is that it emerges precisely when demographic pressures are beginning to reshape developed economies. The US may not face demographic decline on the scale of South Korea, but it confronts many of the same underlying challenges: rising entitlement costs, an aging population, increasing fiscal burdens and an economic model that depends heavily upon continued labor force participation. A society in which millions of households achieve genuine financial independence would alter the balance of power between labor and capital. Workers with substantial savings possess the ability to negotiate, relocate, reduce working hours, reject undesirable employment or leave the workforce entirely. Workers whose wealth has been destroyed by speculative excess possess far fewer options.

This is where the leverage story becomes more than a financial story. Every speculative cycle promises liberation, every bubble convinces participants that traditional constraints no longer apply, every generation discovers a new mechanism through which ordinary people supposedly gain access to effortless wealth. But when these episodes eventually unwind, the losses are rarely distributed equally: large institutions possess diversified assets, sophisticated risk management systems, privileged access to liquidity and the ability to survive volatility, households possess savings. When those savings disappear, they are replenished through labor. The most revealing aspect of the modern leverage boom is therefore not the possibility of extraordinary gains but the certainty that losses, if they occur, will have consequences extending far beyond brokerage accounts. A worker who loses retirement savings must work longer, an individual carrying debt after a market collapse becomes more dependent upon employment, less capable of enduring financial disruption and less willing to challenge unfavorable conditions. Wealth creates options. Losses remove them.

The final irony is that all of this is marketed as a path toward freedom. Financial independence, early retirement, passive income and wealth without labor have become the dominant promises of modern investing culture. But if the leverage-driven structure ultimately proves unsustainable, the outcome may be the precise opposite of what participants expect - rather than producing a generation liberated from economic necessity, it may produce a generation that enters old age with diminished savings, delayed retirement and a greater dependence on wages than before. In that sense, the most important product being created by the modern financial system may not be wealth at all. It may be workers who have no choice but to keep working.