On UK public debt, yields and affordability

The government and Labour MPs seem fascinated by bond yields. They present the fact that UK yields are high is seen as a short cut to arguing that the Government can’t afford the interest rates on bonds and arguing that the last word on the deficit has to be held by the markets.

This article looks at what the ‘yield’ actually is, argues it is the outcome of policy decisions, that rising yields have no effect or at least very little effect on public finances. It also argues that quantitative tightening makes the affordability of the deficit worse and that alternative debt management operations would ease the situation. It also suggests that the credit default swap price is a better indicator of the market assessment of the viability of public finances.

What is a bond?

Firstly, let’s examine what is a government bond also known as Gilts. A government bond is a certificate proving a loan to the government. It is issued with a face value (or principal), a payment schedule (consisting of a payment value, and frequency, usually described as an annual interest rate), and a duration. The payments are often referred to as coupons due to the original paper format of UK government bonds. The government will redeem the bond at the end of its life at its face value. While they have a face value, on issue, the government may receive more or less than the face value of the bond depending on the coupon value, the current market interest rate, itself based on the Bank of England’s interest rate, and the markets expectations of future interest rates.

What is a yield?

The yield is a mathematical relationship between the price and the coupon. The coupon is the periodic payment made to the bondholder i.e. the interest on the loan. Changes in bond yields are in fact a reflection of a change in price. As prices fall, because the coupon payment does not change, the yield increases. If prices rise, then the yield falls.

About 75% of UK debt Is a fixed coupon, a change in price of the bonds does not impact the interest payments made by the government to the bond holders. The remaining 25% are index linked to the RPI, the measure of price inflation, so again, the fiscal deficit does not impact interest payments.

Public Debt Management

National Debt & Inflation

It might be desirable if the government bought back some of these index linked bonds, although they only become a burden during periods of rising inflation. One advantage of having these bonds is that the difference in yield between these inflation-linked gilts and conventional (fixed-rate) gilts of similar maturity provides a market-implied forecast of future RPI inflation. The markets also use interest rate swaps as a means of hedging the inflation risk, and thus exposing the market’s view as to the future rates of inflation.

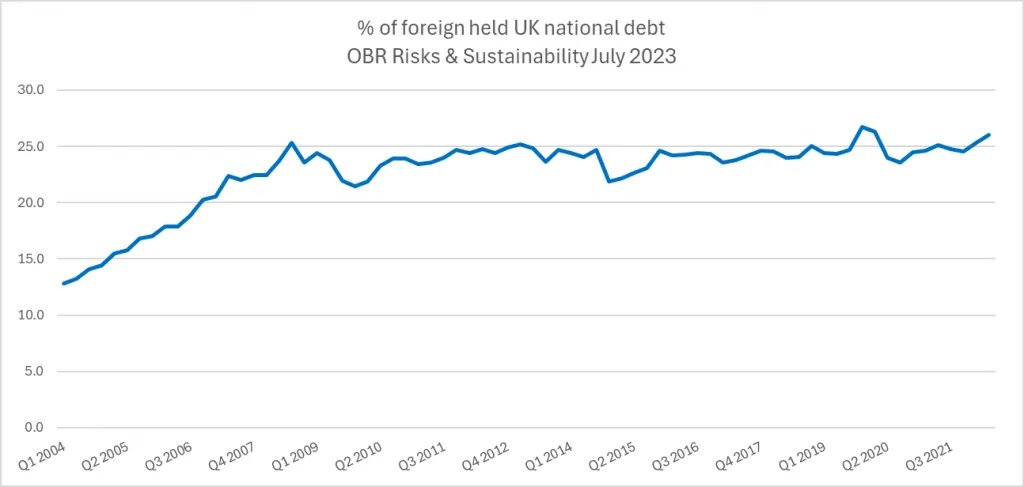

National Debt and price volatility

It might also be useful to buy back [some of] the foreign held bonds at least to manage the ratio. Foreign held debt is also about 25% of the total and is seen as more price sensitive then domestically held debt. The proportion of foreign held government debt has increased significantly over the last twenty years, under the Tories.

Savings and domestic demand

The domestic demand for UK Bonds is based on the ability to save. Richer people save proportionately more than the more numerous poorer parts of society, and they save proportionately more of their incremental income.

It’s hard to disaggregate savings by household income from the data I can find, but easing the cost-of-living crises to allow more people to save, even if only through pensions, would help in creating a domestic demand for government bonds. This policy goal also suggests restricting the amount of cash that can be held in ISAs is a mistake, as it’s simpler to do and the banks will convert such cash holdings into bonds.

Quantitative Tightening

Another problem with government policy is “quantitative tightening”. They are swapping their QE Assets for bank cash and now paying interest on those deposits. i.e. it’s a reverse tax, which subsidises bank profits and reduces the budget “head room” thus squeezing government current account expenditure because of the Chancellor’s “fiscal rules”.

Falling Bond Prices

There is an undesirable impact of falling bond prices. Falling prices impact those organisations who use them as collateral for loans or other transactions requiring it. These are, most visibly, Banks and pension funds and the high cost of getting this wrong was illustrated by the potential crisis the Truss administration.

The Bank of England, presumably, under strong encouragement from the Treasury, the Bank of England is going to reduce the mandatory capital adequacy ratios of the biggest six banks and the Nationwide building society. This needs to be done with care. The thresholds and inspection regime were established during the regulatory reforms after the 2008 crash.

Counter inflation measures

Another problem is that the Government believes that increasing interest rates is counter inflationary. There are two theories as to why this might be so, and one has been discredited, and the other is inappropriate for dealing with cost-push inflation. The first is the Friedmanite quantitative theory of money, that an increase in prices was the result of too much money in the economy and so a counter inflation policy was to increase interest rates to reduce it and/or to use credit controls. Today’s iteration of this theory requires inflation to be stoked by demand, and increasing interest rates, reduces consumer demand, by reducing effective residual disposable income. (This could be done by taxation in which case the Government would get the money, whereas by increasing interest rates, the Banks get it, an adverse policy outcome, compounded by a refusal to levy a banking windfall tax. ) I would also argue that the inflation spike in the Autumn of 2022 was a cost-push spike caused by output shortages caused by COVID and profiteering in the energy sector.

Bankruptcy

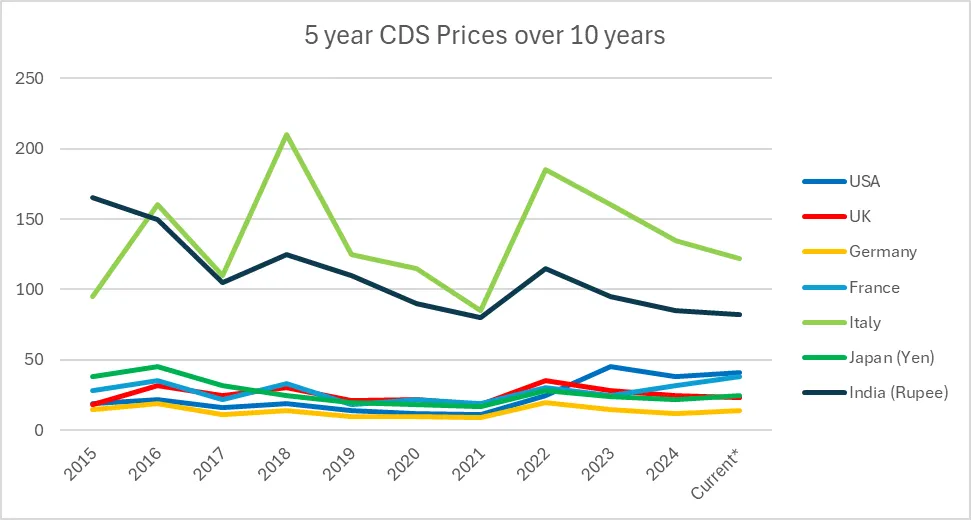

The Government can’t run out of sterling. The true market threat is denial of funds, which is what occurred in Greece. The UK debt to GDP ratio is, just, under 100%. This is low by international standards. The debt to GDP ratio is exceeded by a number of OECD economies. The best measure of this threat would be the sterling credit default swap price which places the likelihood of UK default at ~0.3%. This is good for the leading western economies, again about standard.

From google gemini, https://gemini.google.com/app/9679972ac86a8ddc , they say, a table showing the approximate 5-year Sovereign CDS spreads (in basis points, where 100 bps = 1%) at the end of each year.

The financial rules

Compounding all this deliberate confusion is the deficit fetishism embedded in Reeves’ financial rules. Simon Wren-Lewis, the economist in Corbyn’s leadership team thought to be the most influential supporter of financial rules argues they were needed to protect investment. Reeves’ rules are designed to “break-even” on a yearly budget by the end of the Parliament. The only way this might happen is by growing the economy and increasing the GDP. Even within the constraints of monetarist economics, more relaxed rules could be adopted and as I argue above, the fear of default is infinitesimally low.

If growth is the target, then the key tool for delivering growth should be the Industrial Policy to which I offer a critique an article of the Chartist and summarise on this blog. In that article, I examine the Industrial Policy, praising its comprehensive nature and suggesting that capital mobilisation via the City is unlikely to be successful as it hasn’t been before and that there seems to be a low ability to innovate the economy in the UK. Yet another of the problems with the rules and the failure in the budgets is that GDP growth is dependent on human capital and yet the Government view is that investment in human capital is current account expenditure and is not the focus of education spending. This both embeds a weakness in the policies and illustrates the arbitrary nature of the rules.

Are the bond markets a problem to the Labour Government?

Yes and No, but high yields are not a reasonable factor for determining the deficit.

- Yields are an outcome and caused by changes in price; their impact on the funding the deficit is limited and price changes are not caused by a deficit, but in a limited way by the expectation of inflation.

- The cost of government borrowing is mainly fixed and where variable, is based on the inflation.

- The markets do not consider the governments default risk to be particularly high.

- The debt management policies being pursued are not aimed at reducing the cost of borrowing.

- The so-called rules are the toughest since they were invented as an ideological tool to justify austerity. There’s room to rewrite them.

- The industrial programme is insufficiently activist to repair the economy.

Originally published at https://davelevy.info on January 2, 2026.